Finance

The Basics of Bonds and Fixed Income Investing

By

Reviewed

By Mike steven

The Basics of Bonds and Fixed Income Investing

Investing in bonds and fixed income securities is a cornerstone of conservative investment strategies, providing stability and predictable returns. This article explores the fundamentals of bonds and fixed income investing, breaking down key concepts, types of bonds, and strategies for incorporating them into an investment portfolio.

Image by: https://cdn. pixabay. com

What Are Bonds?

Bonds are debt instruments issued by corporations, governments, or other entities to raise capital. When an investor purchases a bond, they are effectively lending money to the issuer in exchange for periodic interest payments and the return of the principal amount upon maturity. Bonds are a crucial component of fixed income investing, characterized by their regular income streams and lower risk compared to equities.

Key Components of a Bond

- Face Value (Par Value): The amount the bondholder will receive back at maturity. Typically, bonds are issued in denominations of $1,000.

- Coupon Rate: The interest rate paid by the bond issuer on the face value of the bond, usually expressed as an annual percentage. For instance, a bond with a 5% coupon rate and a $1,000 face value will pay $50 annually.

- Maturity Date: The date on which the bond’s principal amount is repaid. Bonds can have short-term (less than 5 years), intermediate-term (5-10 years), or long-term (more than 10 years) maturities.

- Yield: The return on investment for the bondholder, often expressed as a percentage. Yield can be influenced by the bond’s coupon rate, face value, and market price.

Types of Bonds

Understanding the different types of bonds can help investors select the right mix for their portfolios.

- Government Bonds

Government bonds are issued by national governments and are considered low-risk. They are backed by the government’s creditworthiness.

- Treasury Bonds (T-Bonds): Issued by the U.S. Department of the Treasury with maturities ranging from 10 to 30 years.

- Treasury Notes (T-Notes): Shorter maturities compared to T-Bonds, ranging from 2 to 10 years.

- Treasury Bills (T-Bills): Short-term securities with maturities of one year or less.

- Municipal Bonds

Issued by state and local governments, municipal bonds help finance public projects. They come in two main types:

- General Obligation Bonds: Backed by the issuer’s taxing power.

- Revenue Bonds: Supported by the revenue generated from specific projects or sources.

- Corporate Bonds

Issued by corporations to fund business operations, corporate bonds come with varying degrees of risk and yield.

- Investment-Grade Bonds: Issued by financially stable companies, offering lower yields but lower risk.

- High-Yield Bonds (Junk Bonds): Issued by companies with lower credit ratings, offering higher yields to compensate for higher risk.

- Agency Bonds

Issued by government agencies or government-sponsored enterprises (GSEs), such as Fannie Mae or Freddie Mac. They often offer higher yields than government bonds but may carry slightly higher risk.

Analyzing Bond Investments

Investors should evaluate several factors before investing in bonds, including credit risk, interest rate risk, and inflation risk.

Credit Risk

Credit risk refers to the possibility that the bond issuer may default on interest payments or the principal. Credit ratings agencies, such as Moody’s, S&P, and Fitch, provide ratings to assess this risk.

Interest Rate Risk

Interest rate risk involves the potential for bond prices to decline as interest rates rise. As new bonds are issued at higher rates, existing bonds with lower rates become less attractive, leading to a decrease in their market value.

Inflation Risk

Inflation risk is the risk that inflation will erode the purchasing power of the bond’s future cash flows. Bonds with fixed coupon rates may lose value in an inflationary environment, as the real return diminishes.

Strategies for Bond Investing

Effective bond investing involves understanding how different types of bonds can complement each other in a portfolio. Here are some common strategies:

- Laddering

Laddering involves purchasing bonds with varying maturities to manage interest rate risk and maintain liquidity. As bonds in the ladder mature, the proceeds can be reinvested in new bonds at current interest rates.

- Barbell Strategy

The barbell strategy involves investing in short-term and long-term bonds while avoiding intermediate-term bonds. This approach balances the higher yields of long-term bonds with the lower risk and liquidity of short-term bonds.

- Bullet Strategy

In a bullet strategy, an investor holds bonds that mature at the same time, which aligns with specific future financial goals or obligations. This strategy can be useful for funding large expenses or financial milestones.

Comparative Table of Bond Types

| Bond Type | Issuer | Risk Level | Typical Yield | Tax Treatment |

| Treasury Bonds | U.S. Government | Low | Low | Exempt from state and local taxes |

| Municipal Bonds | State/Local Governments | Low to Moderate | Moderate | Exempt from federal income tax |

| Corporate Bonds | Corporations | Moderate to High | Moderate to High | Taxable |

| Agency Bonds | Government Agencies/GSEs | Low to Moderate | Moderate | Varies by agency |

Analysis Table of Key Bond Features

| Feature | Government Bonds | Municipal Bonds | Corporate Bonds | Agency Bonds |

| Safety | High | Moderate | Varies by issuer | Moderate to High |

| Liquidity | High | Moderate to High | Moderate to High | Moderate to High |

| Tax Benefits | None | Tax-exempt interest (federal) | Taxable | Varies by agency |

| Yield | Low | Moderate | Moderate to High | Moderate |

| Duration | Long-term | Varies | Varies | Varies |

Conclusion

Bonds and fixed income investments play a crucial role in diversifying portfolios and managing risk. By understanding the different types of bonds, their features, and associated risks, investors can make informed decisions to achieve their financial goals. Whether aiming for stability, income, or a balance between risk and return, bonds offer a variety of options to fit various investment needs.

Author

When you need help with your Robinhood account, finding the right support option can save you time and make it easier to resolve your issue. Whether you have a question about your account, a transaction, a card, deposits, withdrawals or another Robinhood feature, the company provides several ways to get assistance. If you are searching for how to call Robinhood for support, it is important to use the support options provided through Robinhood’s official channels. This helps ensure that you are following the correct process and reaching the appropriate support team for your particular issue.

This guide explains how Robinhood support works, where to find assistance, what information you may need, and how to prepare before contacting the company.

How Can You Contact Robinhood Support?

Robinhood offers support through its online Help Center and in-app support experience. Depending on your issue and account type, the available support options can vary. The easiest place to begin is the Robinhood app. After signing in, look for the Help or Support section. From there, you can search for your specific problem and review relevant guidance. If additional assistance is available for your issue, Robinhood may provide an option to contact support.

You can also visit Robinhood’s official website and navigate to its Help Center. The online resources cover many common topics, including account access, transfers, deposits, withdrawals, cards, investments, and other account-related questions. When searching for Robinhood customer support, always start with Robinhood’s own website or mobile app so you can follow the most current instructions.

How to Call Robinhood for Support

If your situation requires phone assistance, begin by signing in to your Robinhood account and checking the support options available for your particular issue. The process generally involves:

- Open the Robinhood app or visit the official Robinhood website.

- Sign in to your account.

- Open the Help or Support section.

- Search for the topic related to your problem.

- Review the available troubleshooting information.

- If phone assistance is offered for your issue, follow the instructions provided by Robinhood.

- Complete any requested verification steps before discussing account-specific information.

Support availability can depend on the issue, product, account, and current Robinhood support procedures. For that reason, it is better to check Robinhood directly instead of relying on old contact information found elsewhere online.

Why Use Robinhood’s Official Support Channels?

Financial accounts contain sensitive information, so it is important to be careful when looking for customer support. Using Robinhood’s official app or website allows you to start from a trusted source and follow the support process associated with your account. It also helps you find information that may have changed since older support guides were published. Official support resources can provide assistance with topics such as:

- Account access and login questions

- Identity verification

- Deposits and withdrawals

- Bank transfers

- Stock and ETF questions

- Options-related account issues

- Cryptocurrency features

- Robinhood debit card concerns

- Statements and account information

- Account restrictions

- General technical problems

The right support path depends on the nature of your question. Before attempting to contact support, review the Help Center or in-app Help section to see whether there is a dedicated process for your specific situation.

What Information Should You Have Ready?

Preparing the necessary information before contacting Robinhood can make the process more efficient. You may want to have basic account details available, along with a clear explanation of the problem. If your question involves a particular transaction, note relevant information such as the date, transaction type, and amount. For technical problems, it can also help to record:

- The device you are using

- Your mobile operating system

- The version of the Robinhood app

- Any error message displayed

- When the problem started

- Steps you have already tried

Avoid sharing sensitive account credentials unless Robinhood’s official support process specifically requests information through an appropriate secure method. Your account password and security codes should be treated as private information.

Common Reasons People Contact Robinhood Support

Robinhood users may need assistance for many different reasons. Some questions can be answered quickly through the Help Center, while others may require account-specific support.

Account Login Problems

If you cannot access your account, begin with Robinhood’s account recovery and login guidance. Check that you are using the correct email address or phone number associated with your account and follow the recovery instructions presented by Robinhood. If you believe your account information has been changed without your authorization, use Robinhood’s official account-security process as soon as possible.

Deposit and Withdrawal Questions

Bank transfers can sometimes require additional processing time or verification. If a deposit or withdrawal does not appear as expected, review the transaction status in your account before contacting support. The Help Center may explain expected processing periods and requirements for different types of transfers.

Card Support

Robinhood customers who use an eligible Robinhood card may have questions about transactions, card access, payments, or other card features. For card-specific questions, use the Help section within your Robinhood account. This can help direct you toward the information that applies to your particular card and situation.

Investment and Trading Questions

If you have questions about an order, investment, buying power, account activity, or another trading feature, check the relevant Robinhood educational and support resources first. Some trading questions are product-specific, so selecting the correct Help Center topic can help you reach the most relevant information.

Cryptocurrency Support

Robinhood also provides cryptocurrency-related services. If you have a question about crypto transactions, transfers, availability, or account functionality, look for the appropriate cryptocurrency support topic inside Robinhood’s Help Center. Because features and requirements can change, use the current information presented by Robinhood when researching your issue.

What If You Cannot Find a Phone Support Option?

Not every support question necessarily provides the same contact options. If you do not see a phone option, continue through the Help Center or in-app support flow and select the topic that best matches your problem. Robinhood may provide articles, account-specific guidance, chat or other support options depending on the issue. This is one reason it is useful to avoid relying on contact details published in outdated articles. Support procedures can change, and the most accurate instructions are generally available through your current Robinhood account and the company’s official website.

Tips for Getting Help Faster

A little preparation can make your support experience smoother.

- Describe the problem clearly. Instead of saying that something is “not working,” explain what you expected to happen and what happened instead.

- Include relevant dates. If your question involves a transfer, payment or transaction, provide the relevant date when appropriate.

- Take note of error messages. Exact wording can help support representatives understand technical problems.

- Check the Help Center first. Many common questions already have step-by-step answers.

- Use the app when possible. Being signed in can help you access account-specific support options.

- Protect your account information. Do not share passwords, authentication codes or other highly sensitive credentials unnecessarily.

Final Thoughts

Knowing how to call Robinhood for support can be useful when you need help with an account, transaction, transfer, card, investment feature, or technical issue. The best starting point is Robinhood’s official app or website, where you can sign in, access the Help or Support section, and find the options currently available for your specific situation. Before contacting support, gather relevant information about your issue and avoid sharing sensitive account credentials unnecessarily. Checking the Help Center first may also help you find a faster solution to common questions.

Because customer-support procedures and available contact options can change, always rely on the latest information presented through Robinhood’s official support experience. This gives you the clearest path toward getting assistance with your account.

Author

A reliable box truck is one of the most valuable assets for businesses involved in delivery, moving, logistics, retail distribution, construction, and service industries. Whether you’re launching a new company or expanding an existing fleet, purchasing a commercial box truck can require a significant investment. Fortunately, box truck financing makes it possible to acquire the equipment you need without paying the full purchase price upfront. Instead of tying up valuable working capital, financing allows your business to spread the cost over manageable monthly payments while keeping cash available for fuel, insurance, payroll, maintenance and growth.

At Lewis Capital, we provide nationwide commercial box truck financing for owner-operators, small businesses, and fleet owners. As an experienced box truck financing company, we work with multiple lending partners to help businesses find financing solutions that match their financial profile and long-term goals.

What Is Box Truck Financing?

Box truck financing is a type of commercial financing that enables businesses to purchase new or used box trucks through structured monthly payments instead of paying the full purchase price upfront. Many industries depend on box trucks every day, including:

- Delivery companies

- Moving businesses

- Furniture retailers

- Appliance distributors

- HVAC contractors

- Plumbing companies

- Electrical contractors

- Food and beverage suppliers

- Medical supply companies

- Courier services

Financing allows businesses to start using the truck immediately while preserving cash flow for day-to-day operations.

Businesses Choose Commercial Box Truck Financing

Buying a commercial truck with cash isn’t always the smartest financial decision. Financing provides flexibility that helps businesses continue growing while maintaining healthy working capital. Some of the biggest advantages include keeping business cash available for operational expenses, expanding your fleet without waiting years to save for another vehicle, purchasing higher-quality equipment that supports business growth, and creating predictable monthly payments that make budgeting easier. Whether you’re buying your first truck or adding several vehicles to your fleet, financing can help your business grow at a sustainable pace.

New vs Used Box Truck Financing

Both new and used box trucks offer advantages depending on your business needs. A new box truck typically includes the latest safety technology, improved fuel efficiency, manufacturer warranty coverage, and lower maintenance costs during the first several years of ownership. These benefits often appeal to businesses planning long-term fleet expansion.

A used box truck generally has a lower purchase price, reducing the amount that needs to be financed. This often results in more affordable monthly payments while helping businesses avoid the rapid depreciation that occurs during the first few years of ownership. Many successful transportation companies choose used commercial trucks because they provide dependable performance at a lower overall cost.

Commercial Box Truck Financing Works

The financing process is generally straightforward. First, you’ll choose the commercial box truck that fits your business needs. After submitting a financing application, lenders review factors such as your business information, income, financial history, and details about the vehicle being purchased. Once approved, financing terms are presented for review. After the agreement is completed, funding is arranged, and you can take ownership of your truck. Working with an experienced box truck financing company like Lewis Capital helps simplify this process by giving businesses access to multiple financing options through our lending network.

What Lenders Look for During Approval

Many business owners believe approval depends only on their credit score. In reality, commercial lenders often evaluate several factors together. Common considerations include:

- Personal and business credit history

- Business revenue

- Bank statements

- Time in business

- Industry experience

- Down payment, if required

- Truck age and condition

- Overall financial stability

Every financing application is unique, and lenders evaluate the complete financial picture before making a decision.

Who Can Benefit from Box Truck Financing?

Commercial box truck financing supports businesses in many industries. Owner-operators can finance their first truck without exhausting their savings. Delivery companies can expand their fleets as customer demand increases. Contractors can transport equipment more efficiently. Moving companies can replace aging vehicles with more reliable equipment, while retail businesses can strengthen their distribution capabilities. Regardless of business size, financing helps companies acquire essential equipment while preserving financial flexibility.

Choosing the Right Box Truck Financing Company

Not every lender specializes in commercial vehicle financing. Choosing the right financing partner can make the entire process easier. A reliable box truck financing company should offer experience with commercial transportation financing, access to multiple lending partners, financing for both new and used trucks, competitive financing programs, responsive customer support, and a streamlined application process. Lewis Capital focuses on commercial transportation financing, helping businesses explore financing options that align with their operational goals.

Why Businesses Choose Lewis Capital

At Lewis Capital, we understand that every trucking business has different financing needs. Some businesses are purchasing their first commercial vehicle, while others are expanding nationwide fleets. Our financing specialists work closely with borrowers to identify financing solutions that support their growth objectives. We provide financing for:

- Box trucks

- Semi-trucks

- Commercial trucks

- Owner-operator trucks

- Fleet vehicles

- Commercial trailers

- Heavy equipment

Because we work with multiple lending partners, businesses can explore financing programs that fit a variety of financial situations and business models.

Tips Applying for Commercial Box Truck Financing

Preparing before you apply can improve the financing experience. Before submitting an application, consider reviewing your business finances, gathering recent bank statements, determining your budget, researching the truck you plan to purchase and understanding your expected monthly payment. Taking these steps helps streamline the financing process and allows lenders to evaluate your application more efficiently.

Grow Your Business with Box Truck Financing

Reliable transportation is essential for companies that depend on timely deliveries and dependable service. Waiting until you can pay cash for a commercial truck may slow your business growth and limit new opportunities. With commercial box truck financing, businesses can purchase the equipment they need while maintaining healthy cash flow and investing in future growth.

Whether you’re purchasing your first truck or expanding an existing fleet, Lewis Capital provides financing solutions designed to help businesses move forward with confidence.

Author

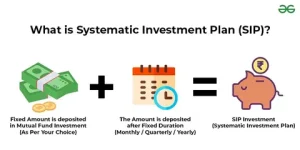

Investing in mutual funds requires strategic thinking. Smart investors constantly seek efficient paths to build long-term wealth. A Systematic Investment Plan represents one of the easiest gateways into the financial markets. Instead of deploying a massive lump sum all at once, you contribute a fixed amount at regular intervals. Most market participants select a monthly schedule. However, certain mutual fund companies also provide a daily contribution option. This choice frequently sparks a compelling debate among retail investors. Both options facilitate regular investing, but they operate on distinct operational timelines. Understanding these operational differences empowers you to make a confident financial choice. Furthermore, examining market mechanics helps you secure a prosperous future.

The Power of Rupee Cost Averaging

Systematic investing introduces a powerful mechanism called rupee cost averaging. When market prices drop, your fixed contribution purchases more units. Conversely, when markets surge, your fixed amount buys fewer units. This dynamic automatically lowers your average purchase cost over time. You eliminate the stressful guesswork of market timing. Investors no longer need to predict market bottoms or tops. Instead, automated contributions smooth out market volatility effortlessly. Market fluctuations actually work in your favor when you maintain a steady contribution rhythm.

Exploring the Mechanics of Monthly Contributions

A monthly systematic plan automates your wealth-building journey completely. The banking system deducts a predetermined amount from your account precisely once every month. You select the exact debit date that matches your financial calendar. For example, you might allocate five thousand rupees every month. The platform invests this full amount on your chosen date without delay. You receive a specific number of units based on the Net Asset Value on that trading day. Monthly schedules dominate the market because they harmonize seamlessly with standard employment salary cycles. Furthermore, investors appreciate how simple it is to track a single monthly transaction on their bank statements. Managing household cash flows becomes remarkably straightforward with a monthly rhythm.

Examining Daily Investment Strategies and Execution

Daily systematic plans function similarly, but they alter the execution frequency dramatically. Instead of a single monthly deduction, the platform executes transactions on every single business day. Suppose you wish to invest five thousand rupees over a monthly cycle. The system divides this total sum into smaller fractional portions. It deploys these micro-portions across every business day of the month. Because market prices fluctuate daily, the Net Asset Value shifts constantly. Consequently, you purchase varying quantities of fund units with each transaction. Selected mutual fund houses offer this feature for individuals who prefer hyper-frequent capital allocations. Technical systems handle these frequent debits seamlessly in the background.

Comparing Operational Frequency: Monthly Versus Daily Systems

The primary distinction between these two options involves operational frequency. A monthly plan deploys your entire capital allocation in one concentrated burst. Conversely, a daily plan distributes that exact same capital across multiple business days. Naturally, a daily schedule generates a much higher volume of transaction records every month. Nevertheless, both systems operate completely automatically once you complete the initial registration process.

Many market commentators claim that daily investing generates superior returns. They argue that spreading purchases across more market levels lowers overall risk. However, historical data invalidates this common assumption. Over extended timeframes, monthly and daily plans produce remarkably similar long-term returns. Market realities rarely favor high-frequency contribution schedules over simple monthly routines.

Dispelling Return Myths and Performance Drivers

Portfolio performance relies on entirely different operational drivers. The specific fund you choose dictates your growth trajectory far more than transaction frequency. Furthermore, broader macroeconomic conditions and your overall investment horizon dictate your final results. Simply increasing transaction frequency does not guarantee enhanced profitability. Market volatility affects all portfolios equally over long holding periods. Therefore, obsessing over daily versus monthly schedules distracts from core wealth-building principles. Successful investing requires patience, disciplined budgeting, and strategic asset allocation rather than tactical frequency tweaks. Expert fund managers emphasize asset quality over transaction timing.

Weighing Convenience and Income Alignment Factors

Convenience remains a critical pillar of personal finance management. Monthly plans offer unmatched simplicity and align perfectly with how employers disburse salaries. Managing a single monthly deduction requires minimal cognitive effort. Daily plans appeal to niche investors who desire hyper-frequent capital deployment. However, daily schedules complicate portfolio tracking and bank statement analysis. Most retail investors find that monthly structures eliminate unnecessary administrative friction. Streamlining your financial life preserves mental energy for other important life tasks. Clear financial records reduce anxiety during tax season and annual reviews.

Navigating Behavioral Finance and Emotional Discipline

Human psychology plays a massive role in successful investing. Emotional panic often triggers poor financial decisions during sudden market downturns. Automated contribution plans remove human emotion from the equation entirely. Whether you choose a monthly or daily schedule, automation enforces strict discipline. You continue buying units even when market news looks bleak. This unwavering consistency separates winning investors from panicked speculators. Trusting the automated process protects your portfolio from emotional interference. Mental resilience fuels long-term financial success.

Selecting the Ideal Systematic Plan for Your Portfolio

Every investor must determine the best approach for their unique financial situation. For the vast majority of individuals, a monthly plan serves as the most practical vehicle. It requires almost zero ongoing maintenance after initial setup. Conversely, a daily schedule works for investors who embrace high-frequency tracking and complex portfolio layouts. Ultimately, investment frequency should never serve as your primary decision criterion. Focus instead on selecting top-tier mutual funds that match your risk tolerance. Allocate a sustainable monthly budget that honors your living expenses. Sound financial planning starts with realistic goals and disciplined execution.

Achieving Long-Term Financial Success Through Consistency

Both monthly and daily systematic plans empower individuals to invest consistently. The core difference simply involves the timing of your capital deployment. Monthly options deploy funds once per cycle, while daily options spread contributions across business days. For most everyday participants, monthly structures deliver optimal convenience and ease of management.

Daily structures accommodate specific preferences, but they rarely create magical return advantages. True financial success stems from disciplined consistency and long-term commitment. Focus on staying invested through market cycles rather than worrying about the exact frequency of your automated contributions. Building lasting wealth is a marathon, not a sprint. Your future self will thank you for maintaining steady financial habits.

Author

Heavy Duty Truck Shop Management Software for Repair Shops

Beckman Adson Retractor for Precision Surgical Procedures

Loverboy Hat: Stylish Streetwear Accessory for Modern Fashion

Thread Lift in Dubai: Benefits, Procedure and Recovery

Perdisco Assignment Help: Expert Support for Accounting Tasks

Selah Clothing, 424 Clothing & Illicit Bloc Luxury Streetwear

TCM Skin Treatment in Dubai for Eczema and Psoriasis Relief

Taghazout Car Rental: Explore Morocco’s Atlantic Coast

How to Call Robinhood for Support: Complete Contact Guide

We Are Righteous Hoodie: Premium Streetwear for Modern Style

Cybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

Meet the Megalodon: The Shark Star of ‘Meg 2’

Reduce Video Game Lag: Level Up Your Gaming Performance

Balancing India’s Entertainment: Cricket vs. Bollywood

Jetsetter’s Secrets: Unveiling Our Favorite Travel Hacks for a Seamless Adventure

The 5 Best Live Sports Streaming Sites: Legal and Exciting!

Hollywood Labor Unrest: The Impact of ‘What About Us?’ Strikes

Unveiling the Magic of Dream Fulfillment at the Late NBA Draft

Illuminate Your Skin: Dr. Axe Unveils Natural Remedies for Lightening Knees and Elbows

Bright Choices: Navigating the Pros and Cons of Skin Whitening Creams with Dr. Axe

-

Business3 years ago

Business3 years agoCybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

-

Entertainment3 years ago

Meet the Megalodon: The Shark Star of ‘Meg 2’

-

Entertainment3 years ago

Reduce Video Game Lag: Level Up Your Gaming Performance

-

Sports3 years ago

Sports3 years agoBalancing India’s Entertainment: Cricket vs. Bollywood

-

Entertainment3 years ago

Jetsetter’s Secrets: Unveiling Our Favorite Travel Hacks for a Seamless Adventure

-

Productivity3 years ago

The 5 Best Live Sports Streaming Sites: Legal and Exciting!

-

Art /Entertainment3 years ago

Hollywood Labor Unrest: The Impact of ‘What About Us?’ Strikes

-

Sports3 years ago

Unveiling the Magic of Dream Fulfillment at the Late NBA Draft