Business

Airtool vs Salesforce: What Growing Businesses Are Choosing

For years, Salesforce dominated conversations around CRM software. And honestly, there’s a reason for that. It became one of the most recognized platforms for managing sales pipelines, customer relationships, reporting, and enterprise workflows at scale. But lately, businesses are asking different questions. That shift is exactly why more businesses are now comparing Airtool vs Salesforce in 2026.

Instead of simply searching for the “biggest CRM,” teams now care more about:

- usability

- workflow simplicity

- operational visibility

- scalability without complexity

Businesses Are Moving Away From Disconnected Systems

Another reason businesses are reconsidering traditional CRM and operational software is the growing demand for flexibility across departments. In many companies, sales teams use one platform, project managers rely on another, operations track workflows somewhere else, and leadership pulls reports from multiple disconnected dashboards. Over time, this creates operational silos that slow down decision-making and reduce visibility across the business.

Teams waste hours switching between systems, updating duplicate records, and manually sharing progress updates that should already be connected automatically. This is where modern platforms are changing expectations. Businesses now want software that can adapt to the way teams actually work instead of forcing employees into rigid structures that become harder to manage as the company scales.

Platforms like Airtool are gaining attention because they approach workflows more holistically. Instead of functioning only as a sales CRM, the platform connects reporting, operations, workflows, task management, and collaboration into one environment. This can greatly ease daily operations and lessen software fatigue, especially for expanding businesses.

Problem Growing Teams Often Face

One thing many businesses don’t realize during implementation is how quickly CRM environments can become difficult to manage.

As more departments, automations, and workflows get added, systems sometimes become:

- overloaded with customizations

- difficult for non-technical users

- expensive to maintain

- heavily dependent on admin support

For smaller and mid-sized businesses especially, this creates friction over time. Employees stop updating information consistently. Teams rely on side spreadsheets again. Reporting becomes inconsistent. Eventually the CRM starts feeling like another operational problem instead of a productivity solution.

Airtool Is Getting Attention

Platforms like Airtool are gaining traction because many businesses now want more than traditional CRM management.

Companies increasingly want:

- CRM

- workflow management

- operations

- reporting

- project coordination

- analytics

inside one connected ecosystem.

Instead of separating operational tools across multiple platforms, Airtool focuses on creating unified workflows that connect different parts of the business together. For growing teams, that operational flexibility can feel easier to manage long term.

Simplicity Is Becoming a Competitive Advantage

One thing I’ve noticed recently is that companies are becoming more cautious about overcomplicating internal systems.

Businesses no longer want software that requires:

- endless onboarding

- constant administration

- complicated updates

- disconnected workflows

They want systems teams can actually use daily without friction. This is where modern operational platforms are changing the conversation.

Instead of selling “more features,” they focus on:

- cleaner workflows

- operational visibility

- collaboration

- scalable processes

- easier adoption across teams

And honestly, that’s becoming far more valuable for many businesses than giant feature lists.

Which Platform Is Better?

The truth is, both platforms serve different types of organizations.

Salesforce may be better for:

- large enterprises

- highly customized sales environments

- complex enterprise reporting

- organizations with dedicated CRM administrators

Airtool may be better for:

- growing operational teams

- businesses wanting unified workflows

- companies reducing software fragmentation

- teams prioritizing usability and flexibility

The right decision depends less on popularity and more on operational fit.

Final Thoughts

The reason businesses are comparing Airtool vs Salesforce in 2026 is simple: Companies are rethinking how CRM systems should function inside modern teams. For years, CRM platforms focused mostly on customer tracking.

Now businesses expect much more:

- workflow automation

- operational visibility

- cross-team collaboration

- scalable systems without chaos

And increasingly, companies are realizing that usability and operational clarity matter just as much as feature depth. Because ultimately, the best CRM is not the one with the most complexity. It’s the one your team actually enjoys using every day because it feels simple, intuitive, and efficient in real workflows. When software reduces friction instead of creating it, employees naturally adopt it without resistance. This leads to better collaboration, fewer errors, improved productivity, and a smoother overall experience across all departments.

Author

Starting a business for the first time can be both exciting and challenging. Many entrepreneurs want to reduce the risks associated with launching a new venture while benefiting from an established business model. This is why franchising has become one of the most attractive investment options in Australia. Buying a franchise allows first-time investors to operate under a recognized brand, receive ongoing support and access proven systems that improve the chances of long-term success.

If you’re considering entering the Australian franchise market, understanding which industries offer the best opportunities is an important first step. Before making your decision, it is also worth exploring the Best Franchise Businesses for Sale in Australia to compare industries, investment levels, and business models that align with your goals.

Why First-Time Investors Choose Franchises

Unlike starting an independent business, a franchise provides a structured path to entrepreneurship. Franchise owners receive operational guidance, marketing support, staff training, and access to an established customer base. For first-time investors, this means spending less time developing business processes and more time focusing on customer service and business growth. Many franchise brands also provide ongoing assistance that helps owners overcome common operational challenges.

Another major advantage is brand recognition. Customers are generally more comfortable purchasing products or services from businesses they already know, making it easier for new franchise owners to build trust within their local market.

What Makes a Franchise a Good Investment?

Not every franchise offers the same level of opportunity. Successful franchises often share several important characteristics:

- A proven and profitable business model

- Strong brand reputation

- Comprehensive franchise training

- Ongoing operational and marketing support

- Sustainable customer demand

- Opportunities for future expansion

Evaluating these factors carefully helps investors choose a business with greater long-term potential.

Top Franchise Opportunities in Australia

Australia offers franchise opportunities across many industries. The following sectors continue to attract entrepreneurs due to their stable demand and growth potential.

Healthcare Franchises

Healthcare continues to be one of Australia’s fastest-growing industries. Increasing health awareness, an ageing population, and rising demand for specialized services create excellent opportunities for investors. Hair restoration franchises such as DHI International represent a specialized healthcare business with global brand recognition, advanced technology, comprehensive franchise training, and growing consumer demand. For entrepreneurs seeking a premium healthcare business, this sector offers significant long-term growth potential.

Home Care Services

Demand for home care and aged care services continues to increase as Australia’s senior population grows. Franchises operating in this sector provide essential services while benefiting from recurring customer relationships.

Cleaning Service Franchises

Residential and commercial cleaning businesses require relatively straightforward operations and serve customers throughout the year. Many investors appreciate the consistent demand and scalable business model offered by cleaning franchises.

Education and Tutoring

Parents continue investing in educational support for children, creating steady demand for tutoring and learning centers. Franchise owners benefit from established teaching systems and recognize educational programs.

Fitness and Wellness

Australians increasingly priorities health and wellness, making fitness centers, personal training studios, and wellness services attractive franchise opportunities. Businesses offering specialized services often experience strong customer retention.

Business Services

Business consulting, printing, digital marketing, and administrative support franchises help other businesses improve efficiency. These franchises often require lower inventory costs while serving a wide range of industries.

How to Evaluate Franchise Opportunities

Before investing, it is important to research every opportunity carefully. Consider the following factors:

- Initial investment requirements

- Franchise fees and ongoing royalties

- Training and operational support

- Brand reputation

- Market demand

- Local competition

- Financial performance

- Growth opportunities

Speaking with existing franchisees can also provide valuable insights into day-to-day operations and the support offered by the franchisor.

Common Mistakes First-Time Franchise Buyers Should Avoid

Many first-time investors make decisions based only on a well-known brand name. However, choosing a franchise requires much more detailed evaluation. Avoid these common mistakes:

- Ignoring total operating costs

- Underestimating working capital requirements

- Failing to understand franchise agreements

- Choosing an industry without researching market demand

- Not comparing multiple franchise opportunities

Taking time to complete proper research reduces investment risk and improves decision-making.

Why Healthcare Franchises Continue to Grow

Healthcare has become one of Australia’s most resilient business sectors. Demand for medical and wellness services remains consistent regardless of economic conditions, making healthcare franchises attractive long-term investments.

Hair restoration has emerged as one of the fastest-growing segments within the healthcare industry. Increasing awareness, technological advancements, and rising consumer demand have created new business opportunities for entrepreneurs seeking specialized healthcare services.

DHI International has established itself as a global leader in hair restoration by offering advanced treatment methods, comprehensive franchise support, and an internationally recognized brand. These qualities make it an appealing choice for investors looking for a healthcare-focused franchise.

Choosing the Right Franchise for Your Goals

Every investor has different objectives, budgets, and experience levels. Some may prefer lower-investment service businesses, while others seek premium healthcare or specialized professional services. Before making a final decision, compare different industries, evaluate franchise support, and review available investment opportunities. A well-researched decision is more likely to deliver sustainable growth and long-term profitability. If you’re exploring available opportunities, reviewing the Best Franchise Businesses for Sale in Australia can help you identify franchises that match your investment goals, industry interests, and long-term business vision.

Conclusion

Franchising offers first-time investors a practical pathway into business ownership by combining proven systems with ongoing support. Whether you are interested in healthcare, education, home services, or business consulting, Australia offers franchise opportunities across a wide range of industries. By carefully evaluating business models, market demand and franchisor support, investors can choose a franchise that aligns with their financial goals and professional aspirations.

Author

Author

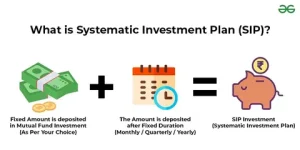

Investing in mutual funds requires strategic thinking. Smart investors constantly seek efficient paths to build long-term wealth. A Systematic Investment Plan represents one of the easiest gateways into the financial markets. Instead of deploying a massive lump sum all at once, you contribute a fixed amount at regular intervals. Most market participants select a monthly schedule. However, certain mutual fund companies also provide a daily contribution option. This choice frequently sparks a compelling debate among retail investors. Both options facilitate regular investing, but they operate on distinct operational timelines. Understanding these operational differences empowers you to make a confident financial choice. Furthermore, examining market mechanics helps you secure a prosperous future.

The Power of Rupee Cost Averaging

Systematic investing introduces a powerful mechanism called rupee cost averaging. When market prices drop, your fixed contribution purchases more units. Conversely, when markets surge, your fixed amount buys fewer units. This dynamic automatically lowers your average purchase cost over time. You eliminate the stressful guesswork of market timing. Investors no longer need to predict market bottoms or tops. Instead, automated contributions smooth out market volatility effortlessly. Market fluctuations actually work in your favor when you maintain a steady contribution rhythm.

Exploring the Mechanics of Monthly Contributions

A monthly systematic plan automates your wealth-building journey completely. The banking system deducts a predetermined amount from your account precisely once every month. You select the exact debit date that matches your financial calendar. For example, you might allocate five thousand rupees every month. The platform invests this full amount on your chosen date without delay. You receive a specific number of units based on the Net Asset Value on that trading day. Monthly schedules dominate the market because they harmonize seamlessly with standard employment salary cycles. Furthermore, investors appreciate how simple it is to track a single monthly transaction on their bank statements. Managing household cash flows becomes remarkably straightforward with a monthly rhythm.

Examining Daily Investment Strategies and Execution

Daily systematic plans function similarly, but they alter the execution frequency dramatically. Instead of a single monthly deduction, the platform executes transactions on every single business day. Suppose you wish to invest five thousand rupees over a monthly cycle. The system divides this total sum into smaller fractional portions. It deploys these micro-portions across every business day of the month. Because market prices fluctuate daily, the Net Asset Value shifts constantly. Consequently, you purchase varying quantities of fund units with each transaction. Selected mutual fund houses offer this feature for individuals who prefer hyper-frequent capital allocations. Technical systems handle these frequent debits seamlessly in the background.

Comparing Operational Frequency: Monthly Versus Daily Systems

The primary distinction between these two options involves operational frequency. A monthly plan deploys your entire capital allocation in one concentrated burst. Conversely, a daily plan distributes that exact same capital across multiple business days. Naturally, a daily schedule generates a much higher volume of transaction records every month. Nevertheless, both systems operate completely automatically once you complete the initial registration process.

Many market commentators claim that daily investing generates superior returns. They argue that spreading purchases across more market levels lowers overall risk. However, historical data invalidates this common assumption. Over extended timeframes, monthly and daily plans produce remarkably similar long-term returns. Market realities rarely favor high-frequency contribution schedules over simple monthly routines.

Dispelling Return Myths and Performance Drivers

Portfolio performance relies on entirely different operational drivers. The specific fund you choose dictates your growth trajectory far more than transaction frequency. Furthermore, broader macroeconomic conditions and your overall investment horizon dictate your final results. Simply increasing transaction frequency does not guarantee enhanced profitability. Market volatility affects all portfolios equally over long holding periods. Therefore, obsessing over daily versus monthly schedules distracts from core wealth-building principles. Successful investing requires patience, disciplined budgeting, and strategic asset allocation rather than tactical frequency tweaks. Expert fund managers emphasize asset quality over transaction timing.

Weighing Convenience and Income Alignment Factors

Convenience remains a critical pillar of personal finance management. Monthly plans offer unmatched simplicity and align perfectly with how employers disburse salaries. Managing a single monthly deduction requires minimal cognitive effort. Daily plans appeal to niche investors who desire hyper-frequent capital deployment. However, daily schedules complicate portfolio tracking and bank statement analysis. Most retail investors find that monthly structures eliminate unnecessary administrative friction. Streamlining your financial life preserves mental energy for other important life tasks. Clear financial records reduce anxiety during tax season and annual reviews.

Navigating Behavioral Finance and Emotional Discipline

Human psychology plays a massive role in successful investing. Emotional panic often triggers poor financial decisions during sudden market downturns. Automated contribution plans remove human emotion from the equation entirely. Whether you choose a monthly or daily schedule, automation enforces strict discipline. You continue buying units even when market news looks bleak. This unwavering consistency separates winning investors from panicked speculators. Trusting the automated process protects your portfolio from emotional interference. Mental resilience fuels long-term financial success.

Selecting the Ideal Systematic Plan for Your Portfolio

Every investor must determine the best approach for their unique financial situation. For the vast majority of individuals, a monthly plan serves as the most practical vehicle. It requires almost zero ongoing maintenance after initial setup. Conversely, a daily schedule works for investors who embrace high-frequency tracking and complex portfolio layouts. Ultimately, investment frequency should never serve as your primary decision criterion. Focus instead on selecting top-tier mutual funds that match your risk tolerance. Allocate a sustainable monthly budget that honors your living expenses. Sound financial planning starts with realistic goals and disciplined execution.

Achieving Long-Term Financial Success Through Consistency

Both monthly and daily systematic plans empower individuals to invest consistently. The core difference simply involves the timing of your capital deployment. Monthly options deploy funds once per cycle, while daily options spread contributions across business days. For most everyday participants, monthly structures deliver optimal convenience and ease of management.

Daily structures accommodate specific preferences, but they rarely create magical return advantages. True financial success stems from disciplined consistency and long-term commitment. Focus on staying invested through market cycles rather than worrying about the exact frequency of your automated contributions. Building lasting wealth is a marathon, not a sprint. Your future self will thank you for maintaining steady financial habits.

Author

Heavy Duty Truck Shop Management Software for Repair Shops

Beckman Adson Retractor for Precision Surgical Procedures

Loverboy Hat: Stylish Streetwear Accessory for Modern Fashion

Thread Lift in Dubai: Benefits, Procedure and Recovery

Perdisco Assignment Help: Expert Support for Accounting Tasks

Selah Clothing, 424 Clothing & Illicit Bloc Luxury Streetwear

TCM Skin Treatment in Dubai for Eczema and Psoriasis Relief

Taghazout Car Rental: Explore Morocco’s Atlantic Coast

How to Call Robinhood for Support: Complete Contact Guide

We Are Righteous Hoodie: Premium Streetwear for Modern Style

Cybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

Meet the Megalodon: The Shark Star of ‘Meg 2’

Reduce Video Game Lag: Level Up Your Gaming Performance

Balancing India’s Entertainment: Cricket vs. Bollywood

Jetsetter’s Secrets: Unveiling Our Favorite Travel Hacks for a Seamless Adventure

The 5 Best Live Sports Streaming Sites: Legal and Exciting!

Hollywood Labor Unrest: The Impact of ‘What About Us?’ Strikes

Unveiling the Magic of Dream Fulfillment at the Late NBA Draft

Illuminate Your Skin: Dr. Axe Unveils Natural Remedies for Lightening Knees and Elbows

Bright Choices: Navigating the Pros and Cons of Skin Whitening Creams with Dr. Axe

-

Business3 years ago

Business3 years agoCybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

-

Entertainment3 years ago

Meet the Megalodon: The Shark Star of ‘Meg 2’

-

Entertainment3 years ago

Reduce Video Game Lag: Level Up Your Gaming Performance

-

Sports3 years ago

Sports3 years agoBalancing India’s Entertainment: Cricket vs. Bollywood

-

Entertainment3 years ago

Jetsetter’s Secrets: Unveiling Our Favorite Travel Hacks for a Seamless Adventure

-

Productivity3 years ago

The 5 Best Live Sports Streaming Sites: Legal and Exciting!

-

Art /Entertainment3 years ago

Hollywood Labor Unrest: The Impact of ‘What About Us?’ Strikes

-

Sports3 years ago

Unveiling the Magic of Dream Fulfillment at the Late NBA Draft