Finance

Examining the Factors Behind First Republic’s Steep Decline in Share Price

First Republic Bank, once a darling of the financial sector, has been faced with a significant decline in share price over recent times. What could be responsible for this trend? Is it due to economic factors or internal issues within the bank itself? Join us as we delve into the root causes behind First Republic’s sharp drop in stock value and explore possible solutions.”

First Republic’s History

First Republic’s history is one of consistent growth and profitability. Founded in 1985, First Republic started out as a small commercial bank in San Francisco. It grew steadily throughout the 1990s and 2000s, opening branches in major cities across the United States. First Republic became known for its high-touch, concierge-style banking services and its strong focus on customer service.

In the past few years, however, First Republic’s share price has declined steeply. The bank has been hit hard by the COVID-19 pandemic, as well as by other macroeconomic factors. In this article, we’ll examine some of the key reasons behind First Republic’s recent struggles.

Recent Financial Struggles

First Republic’s stock price has been in decline since the beginning of 2018. The company has been hit hard by a number of factors, including rising interest rates, slowing loan growth, and declining deposits.

The most significant factor in First Republic’s recent struggles has been the rise in interest rates. The Federal Reserve has raised rates three times since December 2016, and is expected to do so again in 2018. This has put pressure on First Republic’s margins, as the cost of borrowing for the bank has gone up while the yield on its investments has remained relatively static.

To make matters worse, First Republic’s loan growth has slowed significantly in recent quarters. Loan growth was just 5% in the first quarter of 2018, down from 11% in the same quarter last year. This slowdown is likely due to stricter lending standards at the bank as well as a general slowdown in the economy.

Finally, First Republic has also seen its deposits decline in recent months. Deposits fell by 2% in the first quarter of 2018, which puts further pressure on the bank’s funding costs.

All of these factors have combined to create a perfect storm for First Republic, and its share price has reflected this with a steep decline throughout 2018.

The Housing Market

First Republic’s share price has been in decline since the beginning of the year, and this trend continued into the second quarter. The company’s stock is down nearly 40% since the start of 2018. While there are several factors behind this decline, one key reason is the current state of the housing market.

The U.S. housing market has been cooling off in recent months, with sales and prices both declining. This is bad news for First Republic, as a large portion of its business is mortgage lending. The company has already seen a slowdown in its mortgage originations, and a further decline in the housing market could lead to even more loan losses.

In addition to its exposure to the housing market, First Republic is also facing increased competition from other banks and lenders. This is putting pressure on its margins and profitability. First Republic’s shares may continue to decline if these trends persist.

Political Instability

The past year has been a tough one for First Republic Bank (FRC), with the stock down nearly 40%. While part of this can be explained by the broader sell-off in bank stocks, First Republic’s woes are largely of its own making.

First Republic has always been something of a ‘maverick’ bank, eschewing many of the traditional banking practices. This worked well for them during the good times, but has come back to bite them during the current period of political instability.

The bank’s aggressive expansion plans have left it overexposed to some of the more volatile markets, such as San Francisco and Silicon Valley. As these markets have cooled off, First Republic’s loan portfolio has suffered accordingly.

In addition, First Republic’s reliance on high-net-worth individuals makes it particularly vulnerable to any changes in sentiment among this group. And with political uncertainty at home and abroad, there has been a marked decrease in confidence among the wealthy.

First Republic needs to take a more cautious approach in the current environment, which may mean slowing down its expansion plans and increasing its provision for bad loans. Otherwise, it risks further declines in its share price.

Economic Downturn

First Republic’s share price has been in decline since the beginning of the year, and many believe that the current economic downturn is to blame. Let’s take a closer look at the factors behind First Republic’s steep decline in share price.

The first factor to consider is the overall state of the economy. The current economic downturn has led to a decrease in demand for First Republic’s services, as businesses and individuals alike have cut back on spending. This has put pressure on First Republic’s bottom line, and contributed to the decline in its share price.

Another factor to consider is First Republic’s own financial health. The bank has been hit hard by bad loans made during the housing bubble, and has been forced to set aside billions of dollars to cover these losses. This has put a strain on First Republic’s balance sheet, and led investors to question its future profitability.

Finally, it is worth noting that First Republic is not alone in its struggle. Many other banks have also seen their share prices decline sharply this year, as the economic downturn has taken its toll on the financial sector as a whole.

So far this year, First Republic’s stock is down about 35%. While there are many factors at play, it is clear that the current economic environment is putting pressure on First Republic and its shareholders.

What does the future hold for First Republic?

Since its founding in 1985, First Republic has been a leading provider of private banking and wealth management services. However, the company’s share price has declined steeply in recent months, down nearly 50% from its 52-week high.

What is behind this decline? And what does the future hold for First Republic?

There are a number of factors behind First Republic’s share price decline. Firstly, the company has been hit hard by the COVID-19 pandemic, with its business travel and luxury goods businesses particularly affected. Secondly, First Republic has been under pressure from activist investors to improve its governance and financial performance. Thirdly, the company faces stiff competition from other private banks and wealth managers.

Looking to the future, it is difficult to say how First Republic will fare. The company is undoubtedly facing challenges on many fronts. However, it remains a well-respected brand with a strong client base. With the right strategy and execution, First Republic could still turn things around and deliver shareholder value over the long term.

Conclusion

In conclusion, it is clear that First Republic’s steep decline in share price can be attributed to a variety of factors. The company’s financial woes coupled with the general economic downturn due to the pandemic have both played a role in driving down their stock prices. Additionally, their failure to properly manage customer service and product quality issues has resulted in a lack of trust from customers and investors alike. Finally, the emergence of new competitors in the market has further compounded these issues for First Republic. With all this taken into account, it is essential that First Republic act quickly and decisively if they are to turn around their current situation and restore investor confidence.

Author

Running a business is not only about making sales. One of the biggest challenges for MSMEs and small business owners is managing day-to-day expenses properly. Salaries, rent, electricity bills, supplier payments, raw materials — all these costs continue even when customer payments get delayed. That’s where a Working Capital Loan becomes useful.

Many businesses in India use working capital finance to handle short-term business needs and maintain smooth operations without disturbing regular cash flow. Regardless of being a manufacturer, retailer, exporter, trader, or service-oriented firm, working capital assistance enables businesses to maintain operations seamlessly.

This blog will explain what a Working Capital Loan is, how it functions, the different types available, its advantages, and who is eligible to apply for it.

What Is a Working Capital Loan?

A Working Capital Loan is a short-term loan taken by businesses to manage their daily operational expenses.

Unlike long-term business loans that are used for buying machinery, office space, or expansion, a working capital loan is mainly used for routine expenses like:

- Employee salaries

- Rent and utility bills

- Supplier payments

- Purchasing inventory

- Managing seasonal demand

- Handling temporary cash flow gaps

In simple words, it helps businesses maintain regular operations when incoming cash flow is not enough.

For example, if a company has supplied goods to buyers but payment will come after 45 days, the business may still need funds immediately to continue operations. In such situations, working capital finance helps bridge the gap.

Businesses Need Working Capital Loans

Many Indian MSMEs face delayed payments from buyers. At the same time, operational expenses cannot wait.

A Working Capital Loan helps businesses:

- Maintain smooth business operations

- Avoid cash flow shortages

- Continue production or services without interruption

- Handle sudden business expenses

- Manage seasonal sales fluctuations

- Improve business stability

This is the reason why managing working capital is crucial.

How Does a Working Capital Loan Work?

The process is usually simple.

A lender provides a certain amount of money to the business based on factors like:

- Business turnover

- Revenue

- Credit profile

- Repayment history

- Existing business operations

The business can then use these funds for short-term operational requirements.

The repayment may happen through:

- Monthly EMIs

- Flexible withdrawal and repayment structure

- Invoice settlement

- Auto deductions from sales

The loan tenure is generally shorter compared to regular business loans. It can range from a few months to a few years depending on the loan type.

Types of Working Capital Loans

Different businesses have different funding needs. Because of that, lenders offer multiple types of working capital finance options.

1. Term Loan

This is one of the most common forms of working capital loans.

The lender gives a fixed amount to the borrower, and repayment happens through EMIs over a fixed tenure.

Suitable for:

- Short-term operational needs

- Inventory purchase

- Business expansion support

2. Cash Credit Facility

Under this facility, businesses get a borrowing limit from the lender.

Suitable for:

- Businesses with fluctuating cash flow

- Regular working capital requirements

3. Overdraft Facility

An overdraft allows businesses to withdraw more money than the available balance in their current account.

Interest is charged only on the utilized amount.

Suitable for:

- Emergency cash requirements

- Temporary liquidity management

4. Invoice Financing

Many businesses face delayed payments from buyers.

This improves cash flow without waiting for customers to clear payments.

Suitable for:

- MSMEs

- Exporters

- B2B businesses

Who Can Apply for a Working Capital Loan?

Different lenders may have different eligibility criteria, but generally the following businesses can apply:

- MSMEs

- Startups

- Proprietorship firms

- Partnership firms

- Private limited companies

- Traders and retailers

- Manufacturers

- Service providers

Lenders usually check:

- Business vintage

- Annual turnover

- Bank statements

- GST returns

- Credit history

Documents Required for Loan

The documentation process is usually simple.

Common documents include:

- PAN card

- Aadhaar card

- Business registration proof

- GST registration

- Bank statements

- Income tax returns

- Financial statements

- KYC documents

Some lenders may ask for additional documents depending on the loan amount.

Things Businesses Should Consider

Understand the Loan Cost

Check:

- Interest rates

- Processing fees

- Hidden charges

- Penalties

Borrow Only What Is Needed

Taking excessive debt can create repayment pressure later.

Compare Different Lenders

Always compare loan terms before making a decision.

Read Terms Carefully

Understand all conditions before signing the agreement.

Can MSMEs Get Working Loans?

Government initiatives for MSMEs have also improved funding accessibility for small businesses. Still, approval depends on business performance, repayment history, and financial stability.

Final Thoughts

For many businesses, especially MSMEs, managing cash flow is one of the toughest parts of operations. Sales may be growing, but delayed payments and rising expenses can still create pressure.

A Working Capital Loan helps businesses maintain stability during such situations. It supports smooth operations, improves cash flow management, and gives businesses the flexibility to handle short-term financial needs without disrupting daily work. Before taking any loan, businesses should properly assess their requirements, compare options, and choose a financing solution that matches their repayment capacity and operational needs.

Author

Running a small business in India is not easy. Most MSMEs face one common issue — delayed payments from buyers. Sometimes payments get stuck for 30, 60, or even 90 days. At the same time, salaries, costs of raw materials, rent, and GST payments remain due. Invoice trading is currently assisting numerous small businesses. Rather than waiting for clients to settle invoices, companies can sell their outstanding invoices on an invoice trading platform to receive fast funds. It assists in enhancing working capital without obtaining a conventional loan.

Over the last few years, invoice trading has become popular among MSMEs, especially through TReDS platforms in India. In this blog, let’s understand the top benefits of invoice trading and why more businesses are using it to manage cash flow better.

What is Invoice Trading?

Invoice trading is a process where MSMEs can sell their unpaid invoices to financiers or banks and receive early payment. For instance, if your purchaser will settle after 60 days, you don’t have to wait that period. You can submit the invoice on an invoice trading platform, and financiers can finance it after applying a minor discount fee.

It’s an easy method to access cash tied up in receivables.

Invoice trading is commonly used by:

- MSMEs

- Manufacturers

- Suppliers

- Service providers

- Exporters

- Small distributors

Top 10 Benefits of Invoice Trading

1. Improves Cash Flow Quickly

One of the biggest benefits of invoice trading is faster access to working capital.

Many small businesses struggle because money gets blocked in unpaid invoices. Invoice trading converts those invoices into immediate cash.

This helps businesses:

- Pay suppliers on time

- Manage operational expenses

- Handle urgent orders

- Avoid cash crunch situations

Healthy cash flow keeps the business running smoothly.

2. Reduces Dependency on Traditional Loans

Invoice trading is much simpler compared to traditional financing.

Instead of taking a loan, businesses use their existing invoices to get funds. This reduces dependency on:

- Overdraft facilities

- High-interest loans

- Informal borrowing

- Personal funds

It becomes a smarter way to manage working capital.

3. No Need for Heavy Collateral

Most MSMEs face difficulty because banks ask for collateral like property or fixed assets.

With invoice trading, the invoice itself acts as the basis for financing. In many cases, businesses don’t need heavy collateral security.

This is especially useful for:

- New businesses

- Small manufacturers

- Growing startups

- Service-based MSMEs

Businesses can access funds without risking valuable assets.

4. Helps Businesses Accept Bigger Orders

Suppose a large buyer places a big order. The supplier may need immediate money for raw materials, labor, logistics, or production. Invoice trading helps businesses take up larger orders confidently because future receivables can be converted into quick funds. This supports business expansion and growth.

5. Better Working Capital Management

Working capital is the backbone of every small business.

Poor working capital management can affect daily operations, vendor relationships, and even employee salaries.

One of the practical benefits of invoice trading is that businesses can maintain a stable cash cycle.

Instead of waiting for payments, businesses can:

- Rotate money faster

- Improve liquidity

- Plan expenses better

- Reduce payment pressure

This creates better financial discipline over time.

6. Faster Process with Digital Platforms

Traditional financing usually involves paperwork and multiple branch visits.

Today, invoice trading platforms have made the process much faster and digital.

Businesses can:

- Upload invoices online

- Track transactions digitally

- Receive bids from financiers

- Get payments directly in bank accounts

Digital invoice trading saves time and reduces manual hassle.

7. Lower Risk of Payment Delays

Delayed payments are one of the biggest challenges for MSMEs in India.

This gives more financial stability and reduces dependency on payment cycles. It also helps businesses focus more on operations instead of constantly following up for payments.

8. Competitive Financing Rates

Compared to unsecured loans or informal borrowing, trading often comes with better financing rates.

Why?

9.Builds Stronger Supplier and Buyer Relationships

Cash flow problems can impact relationships with vendors and suppliers.

If payments are delayed regularly, trust issues may arise. With trading, businesses get quicker access to funds and can pay suppliers on time.

This helps in:

- Maintaining supplier confidence

- Negotiating better deals

- Building long-term partnerships

- Improving business reputation

Strong financial management creates stronger business relationships.

10. Supports MSME Growth and Stability

Small businesses need consistent liquidity to survive and grow. Invoice trading fosters business expansion by guaranteeing access to funds when necessary.

Businesses can use the money for:

- Hiring staff

- Purchasing inventory

- Expanding operations

- Investing in machinery

- Managing seasonal demand

Why Invoice Trading is Growing in India

India’s MSME sector contributes significantly to the economy, but delayed payments remain a major concern. To enhance MSME funding, platforms within the TReDS ecosystem are assisting companies in obtaining receivables financing more transparently and digitally.

Awareness about invoice trading is increasing because businesses now understand that unpaid invoices are not just pending payments — they are financial assets. More companies are adopting digital financing solutions to improve liquidity and reduce operational stress.

Final Thoughts

For small businesses dealing with delayed receivables, trading can become a practical financial tool instead of relying completely on traditional loans. As more MSMEs adopt digital financing platforms in India, invoice trading is slowly becoming an important part of modern business cash flow management.

Author

Running a business is not only about making sales. One of the biggest challenges for MSMEs and small business owners is managing day-to-day expenses properly. Salaries, rent, electricity bills, supplier payments, raw materials — all these costs continue even when customer payments get delayed. That’s where a Working Capital Loan becomes useful.

Many businesses in India use working capital finance to handle short-term business needs and maintain smooth operations without disturbing regular cash flow. Regardless of being a manufacturing unit, retailer, exporter, trader, or service-oriented business, working capital assistance enables companies to sustain their operations smoothly. In this blog, let’s explore the meaning of a Working Capital Loan, its operation, the various types, advantages, and the eligibility for applicants.

What Is a Working Capital Loan?

A Working Capital Loan is a short-term loan taken by businesses to manage their daily operational expenses.

Unlike long-term business loans that are used for buying machinery, office space, or expansion, a working capital loan is mainly used for routine expenses like:

- Employee salaries

- Rent and utility bills

- Supplier payments

- Purchasing inventory

- Managing seasonal demand

- Handling temporary cash flow gaps

In simple words, it helps businesses maintain regular operations when incoming cash flow is not enough. For example, if a company has supplied goods to buyers but payment will come after 45 days, the business may still need funds immediately to continue operations. In such situations, working capital finance helps bridge the gap.

Businesses Need Working Capital Loans

Many Indian MSMEs face delayed payments from buyers. At the same time, operational expenses cannot wait.

A Working Capital Loan helps businesses:

- Maintain smooth business operations

- Avoid cash flow shortages

- Continue production or services without interruption

- Handle sudden business expenses

- Manage seasonal sales fluctuations

- Improve business stability

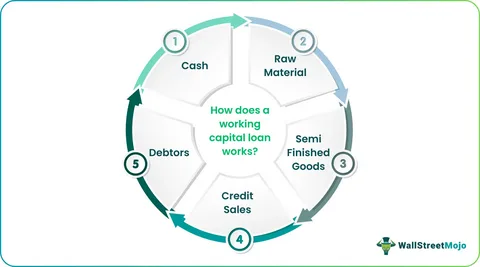

How Does a Working Capital Loan Work?

The process is usually simple.

A lender provides a certain amount of money to the business based on factors like:

- Business turnover

- Revenue

- Credit profile

- Repayment history

- Existing business operations

The business can then use these funds for short-term operational requirements.

The repayment may happen through:

- Monthly EMIs

- Flexible withdrawal and repayment structure

- Invoice settlement

- Auto deductions from sales

The loan tenure is generally shorter compared to regular business loans. It can range from a few months to a few years depending on the loan type.

Types of Working Capital Loans

Different businesses have different funding needs. Because of that, lenders offer multiple types of working capital finance options.

1. Term Loan

This is one of the most common forms of working capital loans. The lender gives a fixed amount to the borrower, and repayment happens through EMIs over a fixed tenure.

Suitable for:

- Short-term operational needs

- Inventory purchase

- Business expansion support

2. Cash Credit Facility

Under this facility, businesses get a borrowing limit from the lender. The firm can take out funds whenever necessary and pay interest solely on the amount utilized.

Suitable for:

- Businesses with fluctuating cash flow

- Regular working capital requirements

3. Overdraft Facility

An overdraft allows businesses to withdraw more money than the available balance in their current account.

Interest is charged only on the utilized amount.

Suitable for:

- Emergency cash requirements

- Temporary liquidity management

4. Invoice Financing

This improves cash flow without waiting for customers to clear payments.

Suitable for:

- MSMEs

- Exporters

- B2B businesses

5. Trade Credit

Suitable for:

- Retailers

- Traders

- Manufacturing businesses

Features of a Working Capital Loan

Here are some common features businesses should know:

Quick Access to Funds

Short-Term Financing

These loans are mainly designed for temporary operational needs.

Flexible Usage

Businesses can use funds for multiple day-to-day requirements.

Secured or Unsecured Options

Some working capital loans require collateral while others are unsecured.

Interest on Utilized Amount

In facilities like cash credit and overdraft, interest applies only on the amount used.

Benefits of Working Capital Loans

Helps Maintain Smooth Operations

Businesses can continue daily operations without worrying about cash shortages.

Better Cash Flow Management

A working capital loan helps businesses manage delayed customer payments effectively.

Supports Business Growth

Companies can accept larger orders, maintain inventory, and expand operations smoothly.

Improves Supplier Relationships

Timely payments help businesses maintain trust with suppliers and vendors.

Handles Seasonal Demand

Businesses with seasonal sales can manage high-demand periods easily.

Who Can Apply for a Loan?

Different lenders may have different eligibility criteria, but generally the following businesses can apply:

- MSMEs

- Startups

- Proprietorship firms

- Partnership firms

- Private limited companies

- Traders and retailers

- Manufacturers

- Service providers

Lenders usually check:

- Business vintage

- Annual turnover

- Bank statements

- GST returns

- Credit history

Documents Required for Loan

The documentation process is usually simple.

Common documents include:

- PAN card

- Aadhaar card

- Business registration proof

- GST registration

- Bank statements

- Income tax returns

- Financial statements

- KYC documents

Some lenders may ask for additional documents depending on the loan amount.

Things Businesses Should Consider

Understand the Loan Cost

Check:

- Interest rates

- Processing fees

- Hidden charges

- Penalties

Borrow Only What Is Needed

Taking excessive debt can create repayment pressure later.

Compare Different Lenders

Always compare loan terms before making a decision.

Check Repayment Capacity

Businesses should ensure stable cash flow for repayment.

Read Terms Carefully

Understand all conditions before signing the agreement.

Can MSMEs Get Loans?

Government initiatives for MSMEs have also improved funding accessibility for small businesses. Still, approval depends on business performance, repayment history, and financial stability.

Final Thoughts

For many businesses, especially MSMEs, managing cash flow is one of the toughest parts of operations. Sales may be growing, but delayed payments and rising expenses can still create pressure.

A Working Capital Loan helps businesses maintain stability during such situations. It supports smooth operations, improves cash flow management, and gives businesses the flexibility to handle short-term financial needs without disrupting daily work.

Before taking any loan, businesses should properly assess their requirements, compare options, and choose a financing solution that matches their repayment capacity and operational needs.

Author

Private Limited Company Compliance: OPC, LLP, AIF & Taxation

Micro needling: RF, PRP, Exosomes, and Custom Treatments

SAP Consulting: Digital Transformation for Modern Enterprises

Percentage to CGPA Calculator: Guide to Converting Grades

PC Bottleneck: Complete Guide to Optimizing System Performance

TheCalculators.net: Your All-in-One Platform for Calculations

Farm Mechanization on Indian Agriculture: Boosting Productivity

Laptop Repair in Alopibagh Prayagraj: Fast & Reliable Service

Korean Co Ord Sets: The Future of Effortless Fashion

Farm Mechanization: Driving the Future of Modern Agriculture

Cybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

Team Communication Software Transforms Operations at Finance Innovate

Project Management Tool Transforms Long Island Business

How Alleviate Poverty Utilized IPPBX’s All-in-One Solution to Transform Lives in New York City

Breast Cancer: The Imperative Role of Mammograms in Screening and Early Detection

Unstoppable Collaboration: D.C.’s Citi Open and Silicon Valley Classic Unite to Propel Women’s Tennis to New Heights

Embracing Renewal: Sizdabedar Celebrations Unite Iranians in New York’s Eisenhower Park

The Benefits of Starting a Side Hustle for Financial Freedom

New Blood Donation Screening Questions What You Need to Know

Stylishly Timeless: The 5 Types of Sandals You Need in Your Closet

-

Business3 years ago

Business3 years agoCybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

-

Business3 years ago

Team Communication Software Transforms Operations at Finance Innovate

-

Business3 years ago

Project Management Tool Transforms Long Island Business

-

Business3 years ago

How Alleviate Poverty Utilized IPPBX’s All-in-One Solution to Transform Lives in New York City

-

health3 years ago

Breast Cancer: The Imperative Role of Mammograms in Screening and Early Detection

-

Sports3 years ago

Unstoppable Collaboration: D.C.’s Citi Open and Silicon Valley Classic Unite to Propel Women’s Tennis to New Heights

-

Art /Entertainment3 years ago

Embracing Renewal: Sizdabedar Celebrations Unite Iranians in New York’s Eisenhower Park

-

Finance3 years ago

The Benefits of Starting a Side Hustle for Financial Freedom