Technology

THG’s Stock Rockets After Confirming Apollo’s Takeover Offer

On April 13th, 2023, The Hut Group (THG) announced that it has accepted a takeover bid from Apollo Global Management, Inc. in a deal worth approximately £6.5 billion. The deal will see THG being taken private, giving Apollo full control of the company.

The announcement of the deal sent THG’s shares soaring by over 20%, reaching a new all-time high. This comes after THG’s shares had already experienced a steady climb over the past few months, following the company’s strong financial performance in 2022.

THG is an e-commerce company that owns and operates a range of brands in the beauty, wellness, and nutrition industries. The company was founded in 2004 by entrepreneur Matthew Moulding and has since grown to become one of the UK’s biggest online retailers, with operations in over 190 countries.

The takeover by Apollo is seen as a significant development for THG, as it will provide the company with the financial backing and resources needed to continue its growth trajectory. In a statement announcing the deal, THG said that the transaction will allow the company to “accelerate its growth plans and continue to invest in its infrastructure, technology, and people.”

The deal is also expected to be beneficial for Apollo, which has been actively seeking opportunities to invest in the e-commerce sector. The private equity firm has a strong track record of investing in companies with high-growth potential and supporting them with resources and expertise to help them achieve their full potential.

While the takeover bid has been welcomed by THG’s board of directors, it still requires the approval of the company’s shareholders. A shareholder vote is expected to take place in the coming weeks, and if approved, the deal is expected to close in the second half of 2023.

The news of THG’s takeover bid by Apollo has received mixed reactions from analysts and investors. Some have praised the deal, citing the potential benefits for both THG and Apollo. Others, however, have expressed concerns about the impact that the takeover could have on THG’s employees and the wider e-commerce industry.

There are also concerns that the takeover bid could trigger a wave of similar deals in the e-commerce sector, as private equity firms and other investors seek to capitalize on the sector’s growth potential. This could lead to a consolidation of the industry, with smaller players being acquired or forced out of the market.

Overall, the THG-Apollo deal represents a significant development in the e-commerce industry and is likely to have far-reaching implications for the sector. As THG continues to grow and expand its operations, it will be interesting to see how the company’s new ownership structure affects its future trajectory.

Author

n today’s digital world, even a minor software vulnerability can expose an entire organization to serious cyber threats. A single insecure line of code can put millions of users and critical data at risk. Because of this growing threat landscape, cybersecurity is no longer just about protecting networks and systems from the outside; it has become a fundamental part of how software itself is built.

The old practice of developing software first and adding Security later is no longer effective. In fact, it often creates more risks than solutions. With major cyber incidents such as the SolarWinds supply chain attack and vulnerabilities like Log4j, organizations have realized that Security must be embedded throughout the entire development process. This is where Secure Software Lifecycle Management (SSLM) plays a crucial role in modern cyber defense.

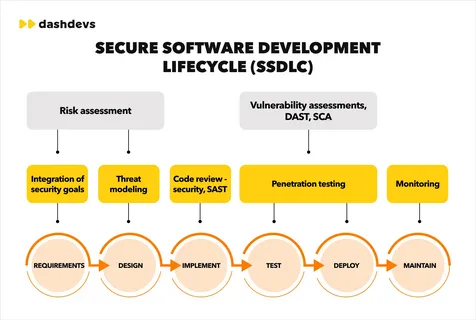

The Shift-Left Approach

Traditionally, security checks were performed only after software development was complete. This resulted in vulnerabilities being identified late in the process, leading to costly and challenging repairs.

Today, organizations are adopting the Shift-Left security approach, integrating security practices into the earliest stages of the Software Development Life Cycle (SDLC). By incorporating security considerations into the planning, design, and coding phases, teams can identify potential weaknesses before they become real problems.

This proactive approach not only reduces costs but also ensures that Security becomes a core part of the software rather than an added feature.

Connecting Development Teams

One of the biggest challenges in modern IT environments is the communication gap between developers and security teams. Developers often prioritize performance, functionality, and speed, while security professionals focus on minimizing risks and vulnerabilities.

Secure Software Lifecycle Management helps bridge this gap by creating a structured framework that enables both teams to collaborate effectively. Certifications such as the Certified Secure Software Lifecycle Professional (CSSLP) equip professionals with the knowledge and methodology to manage Security throughout the software lifecycle—from planning and development to deployment and eventual retirement. Rather than focusing solely on writing secure code, the approach emphasizes managing the entire ecosystem that produces and maintains software.

Securing the Software Supply Chain

Most modern applications are not built entirely from scratch. Developers rely heavily on open-source libraries, third-party frameworks, and external APIs. While these resources accelerate development, they can also introduce hidden security risks.

Secure Software Lifecycle Management ensures that every component used in software development is carefully reviewed, tracked, and monitored for vulnerabilities. Without proper oversight, a single compromised dependency can weaken the Security of the entire application. By implementing structured processes, organizations can maintain greater visibility and control over their software supply chain.

Developing the Next Generation of Security Professionals

As organizations place greater emphasis on secure software development, the demand for skilled cybersecurity professionals continues to grow. Certifications like CSSLP are becoming increasingly valuable for professionals who want to demonstrate expertise in secure software lifecycle practices.

However, mastering the multiple domains covered in the certification requires both theoretical knowledge and practical preparation. Many candidates enhance their preparation through simulation tools that replicate the structure and pressure of the real exam environment. Practice platforms, whether desktop or web-based, allow candidates to test their understanding, identify knowledge gaps, and build confidence before taking the actual certification exam.

Building Skills

As organizations place greater emphasis on secure development practices, the demand for professionals with specialized knowledge continues to grow. Preparing for certifications like CSSLP requires both conceptual understanding and practical exam readiness.

Many candidates improve their preparation by practicing with tools designed to simulate real exam scenarios. For example, using CSSLP Desktop Practice Software allows learners to practice offline in an environment that closely resembles the actual certification exam. This helps them understand the exam structure, manage time effectively, and strengthen their confidence.

At the same time, professionals who prefer flexibility often rely on a CSSLP Web-Based Practice Test, which enables them to practice from any device and continue learning wherever they are. Combining these preparation methods often helps candidates develop a stronger understanding of secure software lifecycle principles.

Security, Compliance, and Business Trust

Secure Software Lifecycle Management is not only important for protecting applications but also for meeting regulatory requirements. Laws and regulations around data protection continue to evolve, and organizations are expected to demonstrate responsible security practices.

Companies that implement secure development processes show customers and partners that they take cybersecurity seriously. In the digital economy, trust plays a major role in long-term business success, and strong security practices help organizations maintain that trust.

Final Thoughts

Cyber defense today starts long before software is deployed. It begins during design discussions, development planning, and coding itself. Organizations that integrate security throughout the entire software lifecycle are better equipped to prevent vulnerabilities and protect their systems from evolving threats.

For developers, security engineers, and project managers, understanding secure software lifecycle management is becoming an essential skill. By prioritizing security from the beginning and continuously improving development practices, organizations can build software that is both innovative and resilient.

Author

When James and Aamir founded their consultancy firm, they shared more than ambition. They shared trust. One brought financial expertise, the other brought industry connections. In the early days, decisions were made over coffee, expenses were tracked in spreadsheets, and profits were divided with a handshake. The business grew quickly. Clients multiplied. Revenue increased. Yet as the numbers became larger, so did the questions. The partnership had momentum, but it lacked structured Partnership Accounting.

- Why did the capital accounts look uneven?

- How were partner drawings affecting overall cash flow?

- Were profits being distributed fairly?

- What were their individual tax liabilities?

What once felt simple became increasingly complex. The absence of clarity began to create hesitation in decision-making. Their story reflects the experience of many partnerships. Growth introduces financial intricacy. Without a solid accounting structure, uncertainty can quietly undermine even the strongest business relationships.

At Lanop Business and Tax Advisors, we believe that effective Partnership Accounting transforms uncertainty into clarity and shared ambition into measurable profit. It is not merely compliance. It is the economic structure that safeguards collaborations, enhances trust, and promotes sustainable development.

The Foundation of Partnership Accounting

Partnership Accounting refers to the structured process of recording, managing, and reporting the financial activities of a business owned by two or more partners. Unlike sole traders or limited companies, partnerships require special attention to equity distribution, profit sharing, capital accounts, and tax obligations.

Each partner may contribute different levels of capital, expertise, and time. Profit-sharing arrangements may vary. Withdrawals may occur throughout the year. Without a defined accounting system, tracking these elements becomes difficult.

The foundation of strong Partnership Accounting includes:

- Accurate recording of capital contributions

- Clear documentation of profit and loss allocation

- Consistent tracking of partner drawings

- Preparation of reliable financial statements

- Compliance with tax regulations

When these elements operate together, the partnership gains financial visibility and operational confidence.

Building Trust Through Transparency

This is the power of structured Partnership Accounting. Transparent reporting reduces disputes. It aligns expectations. It creates a shared understanding of performance. Professional partnership accounting services ensure that transparency becomes standard practice rather than an afterthought. When partners see the same numbers and understand how they are derived, collaboration strengthens.

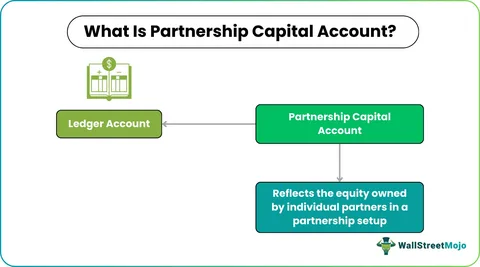

Capital Accounts and Partner Equity

One of the distinguishing features of Partnership Accounting is the management of individual capital accounts. Each partner maintains a capital account reflecting their financial stake in the business.

Capital accounts typically include:

- Initial investment

- Additional contributions

- Allocated profits

- Allocated losses

- Withdrawals

Without careful management, discrepancies can arise. For example, if one partner withdraws more frequently than another, equity balances shift. Inaccurate profit allocation may cause misunderstandings to develop.

Professional partnership bookkeeping records these movements precisely and updates them regularly. This clarity becomes essential during expansion, restructuring, or partner transitions. Capital account accuracy protects both the partnership and the individual partners.

Profit Sharing and Fair Allocation

Profit sharing lies at the heart of partnership relationships. Whether profits are distributed equally or based on agreed ratios, accurate allocation is critical.

Structured Partnership Accounting follows the terms set out in the partnership agreement. This may involve:

- Fixed percentage splits

- Interest on capital contributions

- Salary allowances for active partners

- Performance-related distributions

Errors in profit allocation can have tax consequences and strain relationships. Reliable partnership bookkeeping ensures income and expenses are categorized correctly throughout the financial year, making profit calculation accurate and defensible. When allocation processes are clear and consistent, partners focus on growth rather than disputes.

Role of Partnership Bookkeeping

Behind every strong accounting system lies disciplined daily recording. Partnership bookkeeping forms the operational core of effective financial management. Every invoice issued, every supplier payment, every expense claim, and every partner withdrawal must be recorded accurately. Delayed entries or inconsistent categorization create confusion at year’s end.

Professional partnership bookkeeping provides:

- Real-time tracking of income and expenses

- Accurate reconciliation of bank accounts

- Clear classification of partner drawings

- Reliable data for reporting and analysis

- Reduced risk of costly errors

Consistency in bookkeeping ensures that financial statements reflect reality rather than estimates. At Lanop Business and Tax Advisors, we integrate meticulous partnership bookkeeping within our broader partnership accounting services to provide complete financial oversight.

Tax Responsibilities and Compliance

Partnership taxation requires precision. In many jurisdictions, partnerships operate under pass-through taxation. Profits are allocated to partners who report them individually.

Accurate Partnership Accounting ensures:

- Correct preparation of partnership returns

- Accurate reporting of individual profit shares

- Compliance with regulatory requirements

- Identification of legitimate deductions

- Reduced exposure to penalties

Professional partnership accounting services provide structured support to navigate complex tax rules while maintaining full compliance. Clear documentation protects the partnership during audits and ensures each partner meets their obligations confidently.

Managing Growth and Structural Changes

As partnerships evolve, accounting complexity increases. Growth may require additional capital contributions, financing arrangements, or admission of new partners. Each structural change requires adjustments in capital accounts and profit-sharing ratios. Without organized Partnership Accounting, transitions can become contentious.

Strong partnership financial management ensures smooth integration of new partners, accurate valuation of business interests, and fair settlement of exiting partners. Financial clarity simplifies change management and protects long-term stability.

Why Professional Expertise Matters

While some partnerships attempt internal management, complexity often increases with growth. Regulatory requirements evolve. Tax laws change. Financial risks expand. Engaging experienced advisors ensures that Partnership Accounting remains accurate, compliant, and strategically aligned.

At Lanop Business and Tax Advisors, our approach is comprehensive. We deliver tailored partnership accounting services, structured partnership bookkeeping, and forward-looking partnership financial management designed to protect partner interests and maximize profitability. We understand that each partnership is unique. Our solutions reflect individual goals, industry requirements, and long term ambitions.

Conclusion

Partnerships are built on collaboration, shared responsibility, and collective vision. Yet without structured Partnership Accounting, even strong partnerships may struggle with financial uncertainty. Clear capital accounts, disciplined partnership bookkeeping, transparent profit allocation, and strategic partnership financial management create a stable foundation for growth. When accounting systems are simplified and professionally managed, partners gain clarity, strengthen trust, and unlock sustainable profit.

At Lanop Business and Tax Advisors, we are committed to helping partnerships move from confusion to confidence. Through expert partnership accounting services, we ensure that financial clarity becomes a catalyst for lasting success. Because in every thriving partnership, clarity is not optional. It is essential.

Author

Author

Grand Watches: Heritage, Craftsmanship & Mechanical Mastery

Fear of God Essentials Hoodie: Luxury Streetwear Guide

Chrome Hearts Clothing, Jewelry & Luxury Fashion Guide

Spirit Airlines IAD Terminal Guide: Terminal 1 Services & Tips

Labubu Original: Unique Fashion & Beauty Online Store

Kaftan Sets for Women: Stylish and Comfortable Summer Fashion

Korean Co Ord Sets: Celebrity-Inspired Fashion Trends Guide

Wedding Invitation Designs: Tradition Meets Modern Style

Understanding Child Support in Australia: A Simple Guide

Rudsak Brand: Hoodie & Boots Care, Materials, and Warranty

Cybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

Team Communication Software Transforms Operations at Finance Innovate

Project Management Tool Transforms Long Island Business

How Alleviate Poverty Utilized IPPBX’s All-in-One Solution to Transform Lives in New York City

Breast Cancer: The Imperative Role of Mammograms in Screening and Early Detection

Unstoppable Collaboration: D.C.’s Citi Open and Silicon Valley Classic Unite to Propel Women’s Tennis to New Heights

Embracing Renewal: Sizdabedar Celebrations Unite Iranians in New York’s Eisenhower Park

The Benefits of Starting a Side Hustle for Financial Freedom

New Blood Donation Screening Questions What You Need to Know

Stylishly Timeless: The 5 Types of Sandals You Need in Your Closet

-

Business3 years ago

Business3 years agoCybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

-

Business3 years ago

Team Communication Software Transforms Operations at Finance Innovate

-

Business3 years ago

Project Management Tool Transforms Long Island Business

-

Business3 years ago

How Alleviate Poverty Utilized IPPBX’s All-in-One Solution to Transform Lives in New York City

-

health3 years ago

Breast Cancer: The Imperative Role of Mammograms in Screening and Early Detection

-

Sports3 years ago

Unstoppable Collaboration: D.C.’s Citi Open and Silicon Valley Classic Unite to Propel Women’s Tennis to New Heights

-

Art /Entertainment3 years ago

Embracing Renewal: Sizdabedar Celebrations Unite Iranians in New York’s Eisenhower Park

-

Finance3 years ago

The Benefits of Starting a Side Hustle for Financial Freedom