Finance

Navigating the Investment Landscape: Strategies for Success in a Selective Market

Are you struggling to make the right investments in today’s market? With so many options and a constantly changing economic landscape, it can be tough to know where to put your money. But fear not! This post will provide you with valuable strategies for navigating the investment world successfully. Whether you’re a seasoned investor or just starting out, these tips will help you make informed decisions and see positive returns on your investments. So let’s dive in and discover how to thrive in this selective market!

What is a Selective Market?

A selective market is one where there are fewer opportunities to invest than there are buyers. This can be a good thing if you’re looking for a specific type of investment, but it can also be challenging if you’re not familiar with the available options.

Selective markets can be good or bad for investors. Good because they offer certainty and stability; bad because they may not offer the best return on investment (ROI).

If you’re looking for a stable investment that will provide consistent returns over time, a selective market might be right for you. However, if you’re looking for an opportunity to make quick profits, a selective market might not be the best option. You’ll have to do your research and find investments that are likely to provide high returns.

How to Navigate the Investment Landscape

There is no one-size-fits-all approach to navigating the investment landscape, but following a few key tips can help you make informed decisions that will help you achieve your investment goals.

1. Do Your Homework

Before investing in any particular asset class or security, it’s important to do your research and understand the risks involved. This means not only understanding the company’s financial data and past performance, but also understanding the industry and regulatory environment in which it operates.

2. Stick to Your Routine

When making any investment decision, it’s important to adhere to a consistent process so that you don’t get sidetracked by emotional reactions or external factors. Try not to change your investment strategy based on market conditions – instead, stick with what has worked for you in the past.

3. Diversify Your Holdings

As with anything else in life, it’s always better to be prepared for an adverse event by spreading your risk across several different investments. By diversifying across asset classes and companies, you reduce the chances that a single bad investment will have a significant impact on your overall portfolio performance.

4. Don’t Overreact to Short-term Trends

Even if short-term trends seem compelling at first glance, it’s important to remember that they can often reverse course quickly – so don’t let yourself get too emotionally attached to them. Instead of

What are the Different Types of Investments?

There are a variety of different types of investments that can be made, each with its own set of benefits and drawbacks.

Personal Finance

The first type of investment is personal finance. This includes things like buying stocks, investing in real estate, and saving for retirement. Each option has its own set of benefits and drawbacks. For example, buying stocks can provide the opportunity for quick returns on your investment, but also exposes you to risk if the stock market declines. Investing in real estate can provide stability and a steady stream of income, but it comes with risks such as depreciation and possible tenant defaults. Saving for retirement is an important part of financial planning, but it also comes with risks such as outliving your money or losing your investment if the stock market falls.

Capital Markets

The second type of investment is capital markets. This includes things like buying bonds and mutual funds. Bonds offer stability through periodic payments, while mutual funds allow you to invest in a variety of different stocks and bonds simultaneously. Both options have their own set of benefits and drawbacks. For example, buying bonds offers stability through periodic payments, but they come with a higher interest rate than stock investments. Mutual funds offer diversification through the many different stocks and bonds that they include, but they also come with fees associated with them.

Real Estate

The third type of investment is real estate. This includes things like buying residential or commercial property separately or through real estate Investment trusts (REIT

The Pros and Cons of Each Type of Investment

The Pros and Cons of Each Type of Investment

When it comes to making decisions about which type of investment to choose, there are a number of factors to consider. In this article, we will explore the pros and cons of each major type of investment, and provide strategies for success in a selective market.

Real Estate: Pros

-There is a long history of real estate being one of the most reliable and profitable types of investments. Over time, real estate has consistently provided reliable returns, even during difficult economic times.

-Real estate can be easily liquidated, so it can be quickly converted into cash if needed.

-Real estate is often diversified across many markets, so even if one market begins to decline, there will likely still be other areas where the property is worth investing in.

-Real estate offers the potential for significantreturns over time if done correctly. Cons

-Many people think that real estate is too risky because it’s not backed by anything tangible like stocks or bonds are. This risk can be mitigated by doing your homework and selecting a reputable real estate agent who can help you assess the risks involved in any given property deal.

-Buying a property outright can be expensive, especially in more desirable neighborhoods. The interested buyer may need to put up anywhere from 10% – 30% down on purchase prices typically. This means that they won’t get their money back right away (typically within two years

How to Choose the Right Investments for You

How can you choose the right investments for you, in a selective market? Here are three strategies to help:

1. Understand your risk tolerance. Do you want to take on more risk, or are you happy with lower risks? For example, if you are comfortable with a higher level of risk, then consider investing in stocks that are traded on the stock market. However, if you want lower levels of risk, then invest in bonds or mutual funds that use a less volatile investment method such as stablecoins.

2. Consider your long-term goals. What is your plan for saving for retirement? College tuition? A new car? How much money do you want to save each year and over what period of time? These factors will determine what type of investment is best for you. For instance, if you want to save for retirement over a longer period of time (20 or 30 years), then investing in stocks may not be the best option because they can be risky and volatile. Instead, mutual funds or ETFs that offer stability may be a better fit for your needs.

3. Look at your current financial situation and make sure that the investment is appropriate before making an purchase. Are you able to afford the potential losses associated with an investment? Do you have enough money saved up so that any potential loss won’t impact your overall savings goal? Consider consulting with a financial advisor before making any investment decisions to ensure that the decision is right for you and your specific

Putting It All Together: A Guide to Making Smart Financial Decisions

Investing can be a complex and daunting task, but with the right tools and strategies, it can be an exciting and rewarding experience. In this article, we will outline some key tips for navigating the investment landscape and making smart financial decisions.

1. Understand Your Investment Objectives: When investing, it’s important to remember that your objectives will determine what assets are best suited for you and how aggressively you should invest. If you’re looking to primarily grow your money over time, then stocks may not be the best option for you. On the other hand, if you’re looking to make quick profits or take advantage of short-term opportunities, then high-risk investments such as stocks may be more appropriate.

2. Diversify Your Investments: One of the most important aspects of investing is diversification – spreading your money around a variety of different assets in order to reduce the risk of losing everything if one asset fails. By varying your exposure to different types of investments, you’ll give yourself a better chance of achieving success regardless of what happens in the market.

3. Build A Financial Plan: Another key element of investing is having a financial plan – setting realistic goals and identifying specific methods for reaching them. Without a plan, it’s difficult to know when or how to sell assets or adjust your spending habits in order to reach your targets. Planning also allows you to review your progress on a regular basis and make necessary tweaks as needed.

4. Stay disciplined

Conclusion

In an era of changing markets, it is important for investors to have a clear understanding of how to navigate the investment landscape. This article provides insights into three key strategies for succeeding in selective markets: diversification, risk management and asset allocation. By applying these concepts systematically, investors can maximize their chances of success and avoid common pitfalls that could lead to long-term losses.

Author

Running a business is not only about making sales. One of the biggest challenges for MSMEs and small business owners is managing day-to-day expenses properly. Salaries, rent, electricity bills, supplier payments, raw materials — all these costs continue even when customer payments get delayed. That’s where a Working Capital Loan becomes useful.

Many businesses in India use working capital finance to handle short-term business needs and maintain smooth operations without disturbing regular cash flow. Regardless of being a manufacturer, retailer, exporter, trader, or service-oriented firm, working capital assistance enables businesses to maintain operations seamlessly.

This blog will explain what a Working Capital Loan is, how it functions, the different types available, its advantages, and who is eligible to apply for it.

What Is a Working Capital Loan?

A Working Capital Loan is a short-term loan taken by businesses to manage their daily operational expenses.

Unlike long-term business loans that are used for buying machinery, office space, or expansion, a working capital loan is mainly used for routine expenses like:

- Employee salaries

- Rent and utility bills

- Supplier payments

- Purchasing inventory

- Managing seasonal demand

- Handling temporary cash flow gaps

In simple words, it helps businesses maintain regular operations when incoming cash flow is not enough.

For example, if a company has supplied goods to buyers but payment will come after 45 days, the business may still need funds immediately to continue operations. In such situations, working capital finance helps bridge the gap.

Businesses Need Working Capital Loans

Many Indian MSMEs face delayed payments from buyers. At the same time, operational expenses cannot wait.

A Working Capital Loan helps businesses:

- Maintain smooth business operations

- Avoid cash flow shortages

- Continue production or services without interruption

- Handle sudden business expenses

- Manage seasonal sales fluctuations

- Improve business stability

This is the reason why managing working capital is crucial.

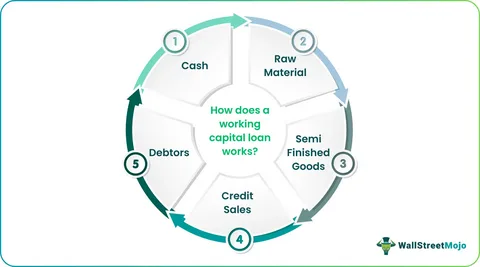

How Does a Working Capital Loan Work?

The process is usually simple.

A lender provides a certain amount of money to the business based on factors like:

- Business turnover

- Revenue

- Credit profile

- Repayment history

- Existing business operations

The business can then use these funds for short-term operational requirements.

The repayment may happen through:

- Monthly EMIs

- Flexible withdrawal and repayment structure

- Invoice settlement

- Auto deductions from sales

The loan tenure is generally shorter compared to regular business loans. It can range from a few months to a few years depending on the loan type.

Types of Working Capital Loans

Different businesses have different funding needs. Because of that, lenders offer multiple types of working capital finance options.

1. Term Loan

This is one of the most common forms of working capital loans.

The lender gives a fixed amount to the borrower, and repayment happens through EMIs over a fixed tenure.

Suitable for:

- Short-term operational needs

- Inventory purchase

- Business expansion support

2. Cash Credit Facility

Under this facility, businesses get a borrowing limit from the lender.

Suitable for:

- Businesses with fluctuating cash flow

- Regular working capital requirements

3. Overdraft Facility

An overdraft allows businesses to withdraw more money than the available balance in their current account.

Interest is charged only on the utilized amount.

Suitable for:

- Emergency cash requirements

- Temporary liquidity management

4. Invoice Financing

Many businesses face delayed payments from buyers.

This improves cash flow without waiting for customers to clear payments.

Suitable for:

- MSMEs

- Exporters

- B2B businesses

Who Can Apply for a Working Capital Loan?

Different lenders may have different eligibility criteria, but generally the following businesses can apply:

- MSMEs

- Startups

- Proprietorship firms

- Partnership firms

- Private limited companies

- Traders and retailers

- Manufacturers

- Service providers

Lenders usually check:

- Business vintage

- Annual turnover

- Bank statements

- GST returns

- Credit history

Documents Required for Loan

The documentation process is usually simple.

Common documents include:

- PAN card

- Aadhaar card

- Business registration proof

- GST registration

- Bank statements

- Income tax returns

- Financial statements

- KYC documents

Some lenders may ask for additional documents depending on the loan amount.

Things Businesses Should Consider

Understand the Loan Cost

Check:

- Interest rates

- Processing fees

- Hidden charges

- Penalties

Borrow Only What Is Needed

Taking excessive debt can create repayment pressure later.

Compare Different Lenders

Always compare loan terms before making a decision.

Read Terms Carefully

Understand all conditions before signing the agreement.

Can MSMEs Get Working Loans?

Government initiatives for MSMEs have also improved funding accessibility for small businesses. Still, approval depends on business performance, repayment history, and financial stability.

Final Thoughts

For many businesses, especially MSMEs, managing cash flow is one of the toughest parts of operations. Sales may be growing, but delayed payments and rising expenses can still create pressure.

A Working Capital Loan helps businesses maintain stability during such situations. It supports smooth operations, improves cash flow management, and gives businesses the flexibility to handle short-term financial needs without disrupting daily work. Before taking any loan, businesses should properly assess their requirements, compare options, and choose a financing solution that matches their repayment capacity and operational needs.

Author

Running a small business in India is not easy. Most MSMEs face one common issue — delayed payments from buyers. Sometimes payments get stuck for 30, 60, or even 90 days. At the same time, salaries, costs of raw materials, rent, and GST payments remain due. Invoice trading is currently assisting numerous small businesses. Rather than waiting for clients to settle invoices, companies can sell their outstanding invoices on an invoice trading platform to receive fast funds. It assists in enhancing working capital without obtaining a conventional loan.

Over the last few years, invoice trading has become popular among MSMEs, especially through TReDS platforms in India. In this blog, let’s understand the top benefits of invoice trading and why more businesses are using it to manage cash flow better.

What is Invoice Trading?

Invoice trading is a process where MSMEs can sell their unpaid invoices to financiers or banks and receive early payment. For instance, if your purchaser will settle after 60 days, you don’t have to wait that period. You can submit the invoice on an invoice trading platform, and financiers can finance it after applying a minor discount fee.

It’s an easy method to access cash tied up in receivables.

Invoice trading is commonly used by:

- MSMEs

- Manufacturers

- Suppliers

- Service providers

- Exporters

- Small distributors

Top 10 Benefits of Invoice Trading

1. Improves Cash Flow Quickly

One of the biggest benefits of invoice trading is faster access to working capital.

Many small businesses struggle because money gets blocked in unpaid invoices. Invoice trading converts those invoices into immediate cash.

This helps businesses:

- Pay suppliers on time

- Manage operational expenses

- Handle urgent orders

- Avoid cash crunch situations

Healthy cash flow keeps the business running smoothly.

2. Reduces Dependency on Traditional Loans

Invoice trading is much simpler compared to traditional financing.

Instead of taking a loan, businesses use their existing invoices to get funds. This reduces dependency on:

- Overdraft facilities

- High-interest loans

- Informal borrowing

- Personal funds

It becomes a smarter way to manage working capital.

3. No Need for Heavy Collateral

Most MSMEs face difficulty because banks ask for collateral like property or fixed assets.

With invoice trading, the invoice itself acts as the basis for financing. In many cases, businesses don’t need heavy collateral security.

This is especially useful for:

- New businesses

- Small manufacturers

- Growing startups

- Service-based MSMEs

Businesses can access funds without risking valuable assets.

4. Helps Businesses Accept Bigger Orders

Suppose a large buyer places a big order. The supplier may need immediate money for raw materials, labor, logistics, or production. Invoice trading helps businesses take up larger orders confidently because future receivables can be converted into quick funds. This supports business expansion and growth.

5. Better Working Capital Management

Working capital is the backbone of every small business.

Poor working capital management can affect daily operations, vendor relationships, and even employee salaries.

One of the practical benefits of invoice trading is that businesses can maintain a stable cash cycle.

Instead of waiting for payments, businesses can:

- Rotate money faster

- Improve liquidity

- Plan expenses better

- Reduce payment pressure

This creates better financial discipline over time.

6. Faster Process with Digital Platforms

Traditional financing usually involves paperwork and multiple branch visits.

Today, invoice trading platforms have made the process much faster and digital.

Businesses can:

- Upload invoices online

- Track transactions digitally

- Receive bids from financiers

- Get payments directly in bank accounts

Digital invoice trading saves time and reduces manual hassle.

7. Lower Risk of Payment Delays

Delayed payments are one of the biggest challenges for MSMEs in India.

This gives more financial stability and reduces dependency on payment cycles. It also helps businesses focus more on operations instead of constantly following up for payments.

8. Competitive Financing Rates

Compared to unsecured loans or informal borrowing, trading often comes with better financing rates.

Why?

9.Builds Stronger Supplier and Buyer Relationships

Cash flow problems can impact relationships with vendors and suppliers.

If payments are delayed regularly, trust issues may arise. With trading, businesses get quicker access to funds and can pay suppliers on time.

This helps in:

- Maintaining supplier confidence

- Negotiating better deals

- Building long-term partnerships

- Improving business reputation

Strong financial management creates stronger business relationships.

10. Supports MSME Growth and Stability

Small businesses need consistent liquidity to survive and grow. Invoice trading fosters business expansion by guaranteeing access to funds when necessary.

Businesses can use the money for:

- Hiring staff

- Purchasing inventory

- Expanding operations

- Investing in machinery

- Managing seasonal demand

Why Invoice Trading is Growing in India

India’s MSME sector contributes significantly to the economy, but delayed payments remain a major concern. To enhance MSME funding, platforms within the TReDS ecosystem are assisting companies in obtaining receivables financing more transparently and digitally.

Awareness about invoice trading is increasing because businesses now understand that unpaid invoices are not just pending payments — they are financial assets. More companies are adopting digital financing solutions to improve liquidity and reduce operational stress.

Final Thoughts

For small businesses dealing with delayed receivables, trading can become a practical financial tool instead of relying completely on traditional loans. As more MSMEs adopt digital financing platforms in India, invoice trading is slowly becoming an important part of modern business cash flow management.

Author

Running a business is not only about making sales. One of the biggest challenges for MSMEs and small business owners is managing day-to-day expenses properly. Salaries, rent, electricity bills, supplier payments, raw materials — all these costs continue even when customer payments get delayed. That’s where a Working Capital Loan becomes useful.

Many businesses in India use working capital finance to handle short-term business needs and maintain smooth operations without disturbing regular cash flow. Regardless of being a manufacturing unit, retailer, exporter, trader, or service-oriented business, working capital assistance enables companies to sustain their operations smoothly. In this blog, let’s explore the meaning of a Working Capital Loan, its operation, the various types, advantages, and the eligibility for applicants.

What Is a Working Capital Loan?

A Working Capital Loan is a short-term loan taken by businesses to manage their daily operational expenses.

Unlike long-term business loans that are used for buying machinery, office space, or expansion, a working capital loan is mainly used for routine expenses like:

- Employee salaries

- Rent and utility bills

- Supplier payments

- Purchasing inventory

- Managing seasonal demand

- Handling temporary cash flow gaps

In simple words, it helps businesses maintain regular operations when incoming cash flow is not enough. For example, if a company has supplied goods to buyers but payment will come after 45 days, the business may still need funds immediately to continue operations. In such situations, working capital finance helps bridge the gap.

Businesses Need Working Capital Loans

Many Indian MSMEs face delayed payments from buyers. At the same time, operational expenses cannot wait.

A Working Capital Loan helps businesses:

- Maintain smooth business operations

- Avoid cash flow shortages

- Continue production or services without interruption

- Handle sudden business expenses

- Manage seasonal sales fluctuations

- Improve business stability

How Does a Working Capital Loan Work?

The process is usually simple.

A lender provides a certain amount of money to the business based on factors like:

- Business turnover

- Revenue

- Credit profile

- Repayment history

- Existing business operations

The business can then use these funds for short-term operational requirements.

The repayment may happen through:

- Monthly EMIs

- Flexible withdrawal and repayment structure

- Invoice settlement

- Auto deductions from sales

The loan tenure is generally shorter compared to regular business loans. It can range from a few months to a few years depending on the loan type.

Types of Working Capital Loans

Different businesses have different funding needs. Because of that, lenders offer multiple types of working capital finance options.

1. Term Loan

This is one of the most common forms of working capital loans. The lender gives a fixed amount to the borrower, and repayment happens through EMIs over a fixed tenure.

Suitable for:

- Short-term operational needs

- Inventory purchase

- Business expansion support

2. Cash Credit Facility

Under this facility, businesses get a borrowing limit from the lender. The firm can take out funds whenever necessary and pay interest solely on the amount utilized.

Suitable for:

- Businesses with fluctuating cash flow

- Regular working capital requirements

3. Overdraft Facility

An overdraft allows businesses to withdraw more money than the available balance in their current account.

Interest is charged only on the utilized amount.

Suitable for:

- Emergency cash requirements

- Temporary liquidity management

4. Invoice Financing

This improves cash flow without waiting for customers to clear payments.

Suitable for:

- MSMEs

- Exporters

- B2B businesses

5. Trade Credit

Suitable for:

- Retailers

- Traders

- Manufacturing businesses

Features of a Working Capital Loan

Here are some common features businesses should know:

Quick Access to Funds

Short-Term Financing

These loans are mainly designed for temporary operational needs.

Flexible Usage

Businesses can use funds for multiple day-to-day requirements.

Secured or Unsecured Options

Some working capital loans require collateral while others are unsecured.

Interest on Utilized Amount

In facilities like cash credit and overdraft, interest applies only on the amount used.

Benefits of Working Capital Loans

Helps Maintain Smooth Operations

Businesses can continue daily operations without worrying about cash shortages.

Better Cash Flow Management

A working capital loan helps businesses manage delayed customer payments effectively.

Supports Business Growth

Companies can accept larger orders, maintain inventory, and expand operations smoothly.

Improves Supplier Relationships

Timely payments help businesses maintain trust with suppliers and vendors.

Handles Seasonal Demand

Businesses with seasonal sales can manage high-demand periods easily.

Who Can Apply for a Loan?

Different lenders may have different eligibility criteria, but generally the following businesses can apply:

- MSMEs

- Startups

- Proprietorship firms

- Partnership firms

- Private limited companies

- Traders and retailers

- Manufacturers

- Service providers

Lenders usually check:

- Business vintage

- Annual turnover

- Bank statements

- GST returns

- Credit history

Documents Required for Loan

The documentation process is usually simple.

Common documents include:

- PAN card

- Aadhaar card

- Business registration proof

- GST registration

- Bank statements

- Income tax returns

- Financial statements

- KYC documents

Some lenders may ask for additional documents depending on the loan amount.

Things Businesses Should Consider

Understand the Loan Cost

Check:

- Interest rates

- Processing fees

- Hidden charges

- Penalties

Borrow Only What Is Needed

Taking excessive debt can create repayment pressure later.

Compare Different Lenders

Always compare loan terms before making a decision.

Check Repayment Capacity

Businesses should ensure stable cash flow for repayment.

Read Terms Carefully

Understand all conditions before signing the agreement.

Can MSMEs Get Loans?

Government initiatives for MSMEs have also improved funding accessibility for small businesses. Still, approval depends on business performance, repayment history, and financial stability.

Final Thoughts

For many businesses, especially MSMEs, managing cash flow is one of the toughest parts of operations. Sales may be growing, but delayed payments and rising expenses can still create pressure.

A Working Capital Loan helps businesses maintain stability during such situations. It supports smooth operations, improves cash flow management, and gives businesses the flexibility to handle short-term financial needs without disrupting daily work.

Before taking any loan, businesses should properly assess their requirements, compare options, and choose a financing solution that matches their repayment capacity and operational needs.

Author

Working Capital Loan: Meaning, Benefits & Types

Bottega Desires Shorts: Streetwear Redefined with Premium Style

Mr. Winston Official Store: Comfortable, and Affordable Streetwear

Mr. Winston Hoodie: Where Style Meets Comfort

Comme des Garçons Limited Edition Drops: Streetwear Influence

Handcrafted Interior Design: Elevating Modern Spaces with Texture

Parquet Flooring: Elegant, Durable, and Stylish Wooden Flooring

Hair Transplant: Advanced Techniques for Natural Results

Dental Implant Drill: Precision, Design, and Material

Hair Transplant Cost in Dubai: Complete Guide to Pricing

Cybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

Team Communication Software Transforms Operations at Finance Innovate

Project Management Tool Transforms Long Island Business

How Alleviate Poverty Utilized IPPBX’s All-in-One Solution to Transform Lives in New York City

Breast Cancer: The Imperative Role of Mammograms in Screening and Early Detection

Unstoppable Collaboration: D.C.’s Citi Open and Silicon Valley Classic Unite to Propel Women’s Tennis to New Heights

Embracing Renewal: Sizdabedar Celebrations Unite Iranians in New York’s Eisenhower Park

The Benefits of Starting a Side Hustle for Financial Freedom

New Blood Donation Screening Questions What You Need to Know

Stylishly Timeless: The 5 Types of Sandals You Need in Your Closet

-

Business3 years ago

Business3 years agoCybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

-

Business3 years ago

Team Communication Software Transforms Operations at Finance Innovate

-

Business3 years ago

Project Management Tool Transforms Long Island Business

-

Business3 years ago

How Alleviate Poverty Utilized IPPBX’s All-in-One Solution to Transform Lives in New York City

-

health3 years ago

Breast Cancer: The Imperative Role of Mammograms in Screening and Early Detection

-

Sports3 years ago

Unstoppable Collaboration: D.C.’s Citi Open and Silicon Valley Classic Unite to Propel Women’s Tennis to New Heights

-

Art /Entertainment3 years ago

Embracing Renewal: Sizdabedar Celebrations Unite Iranians in New York’s Eisenhower Park

-

Finance3 years ago

The Benefits of Starting a Side Hustle for Financial Freedom