health

Understanding Therapy Coverage: Does Insurance Provide Support

Introduction

Insurance coverage for therapy can vary depending on several factors, including the type of insurance plan you have, the specific mental health services you need, and the terms and conditions of your policy. Here are key points to consider:

Key Points Of Insurance Cover Therapy

This image is taken from google.com

- Health Insurance Plans: Many health insurance plans offer coverage for mental health services, including therapy. These plans can be obtained through employers, private insurers, government programs like Medicaid or Medicare, or individual marketplaces.

- Types of Therapy Covered: Different insurance plans may cover various types of therapy, such as individual therapy, group therapy, couples therapy, or family therapy. The coverage may also depend on the therapeutic approach or modality, such as cognitive-behavioral therapy or psychoanalysis.

- In-Network vs. Out-of-Network Providers: Insurance plans often distinguish between in-network and out-of-network providers. In-network therapists have agreements with the insurance company, resulting in lower costs for you. Out-of-network providers may still be covered, but your out-of-pocket expenses could be higher.

- Coverage Limits: Insurance plans may have limits on the number of therapy sessions covered per year or per condition. It’s essential to check your plan’s benefits and limitations to understand how much therapy is covered.

- Authorization and Referral: Some insurance plans require pre-authorization or a referral from a primary care physician before covering therapy services. Make sure to understand and follow the necessary procedures outlined by your insurance plan.

- Co-Payments and Deductibles: Even with insurance coverage, you may still be responsible for co-payments or meeting a deductible before the insurance coverage kicks in. These costs can vary depending on your specific plan.

- Out-of-Pocket Costs: It’s crucial to be aware of any out-of-pocket costs associated with therapy, such as co-payments, co-insurance, or deductibles. Understanding these costs helps you budget for your mental health care.

- Specialized Therapies: Some specialized therapies or practitioners may not be covered by insurance. Examples include certain alternative or holistic therapies. It’s essential to verify coverage for specific therapies with your insurance provider.

Conclusion

This image is taken from google.com

To get accurate and detailed information about your insurance coverage for therapy, consider contacting your insurance company directly. You can find the relevant information in your insurance policy documents, or you can call the customer service number on the back of your insurance card to inquire about mental health coverage and therapy options.

Author

Author

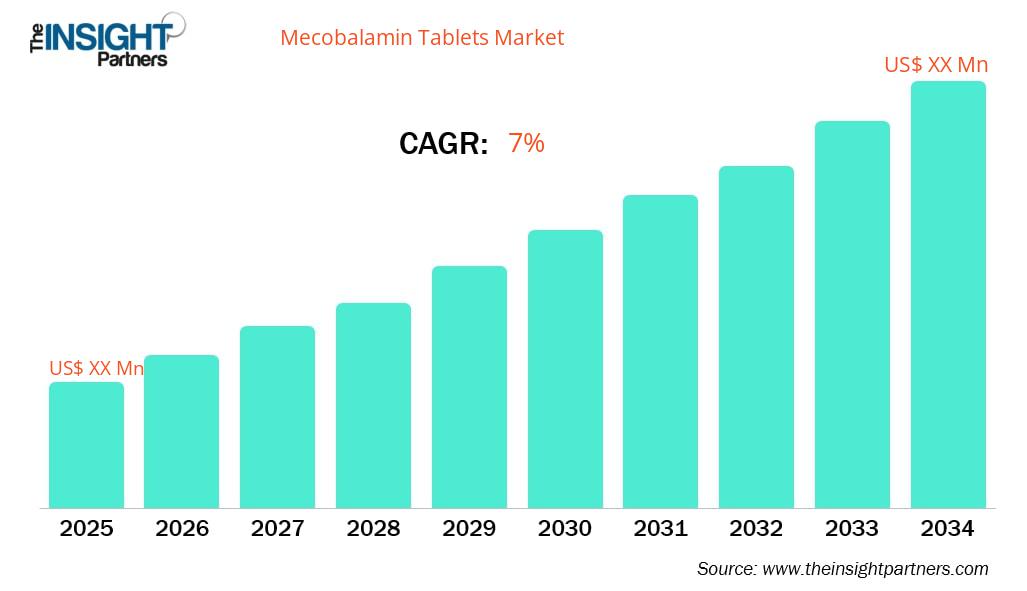

The global pharmaceutical landscape in 2026 has officially entered a “compliance-driven” era. Industry experts now focus on high-precision therapeutic interventions rather than simple supplementation. At the heart of this shift lies the Mecobalamin Tablets Market. Analysts anticipate that this market will expand at a steady compound annual growth rate (CAGR) of 7% through 2034. This growth trajectory reflects a fundamental change in global health priorities. Specifically, the world is now prioritizing neurological preservation and age-related nutritional support.

Mecobalamin is the biologically active coenzyme form of Vitamin B12. It has moved far beyond the “multivitamin” category. Today, clinicians recognize it as a critical medical tool for repairing nerve damage and maintaining cognitive health. This report explores the various catalysts—from demographic shifts to digital health innovations—that drive this market toward its 2034 benchmarks.

The Primary Catalyst: The “Age Wall” and Malabsorption

The most significant factor driving the mecobalamin market over the next decade is the undeniable reality of a rapidly aging global population. By 2030, the World Health Organization predicts that one in six people worldwide will be aged 60 or older. This population will grow from 1 billion in 2020 to approximately 1.4 billion by the end of the decade. This demographic shift creates a direct and massive demand for mecobalamin for two primary biological reasons:

1. Decreased Intrinsic Factor

As individuals age, the body naturally loses its ability to produce intrinsic factor. This protein is necessary for absorbing Vitamin B12 from food sources. This decline leads to a higher prevalence of malabsorption-related deficiencies among seniors. Even those with a balanced diet often cannot extract enough B12 to maintain basic health.

2. Neurological Vulnerability

Age-related health conditions make the elderly more prone to peripheral neuropathy and cognitive decline. Mecobalamin facilitates the synthesis of the myelin sheath, which acts as the protective coating for nerves. Consequently, doctors now use it as a standard-of-care prescription. It helps prevent irreversible structural brain damage and maintains patient mobility as they age.

Leading pharmaceutical stakeholders increasingly prioritize “Compliance Checks.” They want to ensure these life-saving tablets reach aging populations in both developed and emerging markets without delay.

Diabetic Neuropathy: A Growing Clinical Necessity

In 2026, chronic lifestyle diseases continue to act as secondary engines for market expansion. Most notably, type 2 diabetes remains a global crisis. Diabetic neuropathy is a painful complication characterized by nerve damage in the extremities. It affects nearly 50% of long-term diabetic patients. Recent data shows that 38.4 million Americans alone live with diabetes, and half of them will likely develop neuropathy during their lifetime.

Unlike synthetic cyanocobalamin, mecobalamin offers immediate cellular availability. The body does not need to convert it first. This “technical advantage” allows for faster nerve regeneration and more effective pain management. As the global diabetic population scales—particularly in Southeast Asia and North America—healthcare providers will intensify their reliance on high-bioavailability mecobalamin formulations. This clinical need directly supports the projected 7% growth rate.

Market Segmentation: From Hospitals to the Digital Front Door

The market’s structure in 2026 reflects how consumers and clinicians access these treatments. The segmentation of the mecobalamin market highlights a move toward decentralized healthcare:

| Segment Category | 2026–2034 Focus Areas |

| Therapeutic Use | Peripheral Neuropathy, Diabetic Neuropathy, Pernicious Anemia, Dietary Supplement |

| Distribution Channel | Hospital Pharmacy, Retail Pharmacy, Online Pharmacy (Fastest Growing) |

| Formulation | Immediate Release, Sustained Release (Improved Compliance) |

The Online Pharmacy segment is witnessing a massive surge in 2026. “Digital Health” trends drive this growth. Telemedicine platforms now allow patients to receive a diagnosis and a doorstep delivery of their supplements in a single, seamless interaction. For chronic conditions requiring long-term use, the convenience of subscription-based tablet delivery significantly improves patient adherence rates.

The Rise of the “Preventive” Consumer

A fascinating trend emerging in the 2026 market involves the shifting consumer profile. While the elderly remain the primary users, a growing “Preventive” segment among younger professionals (ages 25–45) has emerged.

This shift stems largely from the global mainstreaming of plant-based and vegan diets. In India alone, over 650 million people suffer from Vitamin B12 deficiency due to dietary habits. Since animal products provide almost all dietary Vitamin B12, those following a strict vegan lifestyle face a 100% dependency on supplementation.

Consumers now choose mecobalamin tablets as the “clean label” option. They perceive them as more natural and effective than synthetic alternatives. This proactive approach to health—treating the body before a deficiency becomes a crisis—contributes significantly to the market’s long-term stability. The vegan vitamin B12 market itself is projected to expand at a CAGR of 12% through 2032, highlighting the strength of this demographic.

Overcoming Logistics and Fraud: The Trust Factor

As the market grows, so do the challenges of global supply chain management. In 2026, port congestion and shifting maritime routes make “Logistics Resilience” a major competitive advantage. The best exporters of pharmaceutical-grade mecobalamin maintain priority booking status. They ensure that temperature-sensitive products do not sit in “dwell time” at major ports like Yokohama or Nagoya.

Furthermore, the industry actively combats the risk of counterfeit supplements through Independent Verification. Every batch of premium mecobalamin now undergoes rigorous third-party testing. These tests guarantee potency and purity. This transparency provides the primary “trust signal” for international buyers. They increasingly worry about under-dosed products in the unorganized sector.

After-Sales and The Future of Personalized Medicine

The relationship between pharmaceutical providers and the market no longer ends at the point of sale. By 2030, we expect to see a “Global Service Bridge.” This is where mecobalamin therapy integrates directly into personalized medicine.

Advancements in Nutrigenomics—the study of how genes interact with nutrients—now allow for tailored care. Doctors can prescribe specific mecobalamin dosages based on a patient’s unique genetic ability to process B vitamins. This level of “lifecycle management” ensures that each individual receives an optimized treatment. This trend further solidifies the tablet form as the cornerstone of long-term neurological care.

Conclusion: A Benchmark for 2034

The Mecobalamin Tablets Market is currently navigating a period of profound transformation. The dual pressures of an aging society and a global shift toward preventive wellness drive this change. The industry no longer just sells a vitamin. It provides a critical infrastructure for human longevity.

With a projected 7% CAGR, the next decade will likely see mecobalamin become a standard inclusion in both geriatric care and modern dietary regimens. As long as stakeholders continue to prioritize technical verification and regulatory compliance, the market will remain a vital pillar of the global healthcare economy.

Author

The landscape of metabolic health is shifting from “eat less” to “understand biology.” For residents in the UAE dealing with persistent weight issues or insulin resistance, Mounjaro in Dubai represents the cutting edge of this transition. This advanced treatment is not merely a weight loss aid; it is a sophisticated hormonal regulator designed to correct the physiological signals that often fail in chronic obesity and metabolic syndrome.

In our clinical experience, many patients have spent years fighting their own biology. Mounjaro in Dubai provides a medical “reset,” allowing the body to respond correctly to nutritional intake and satiety cues. By addressing the root causes of metabolic dysfunction, this therapy offers a more sustainable path than traditional methods.

What patients typically report during recovery—which in this case refers to the adaptation period after starting the medication—is a newfound sense of control over food choices and a significant reduction in metabolic noise.

Defining the Dual-Agonist Approach

Mounjaro (tirzepatide) is pioneering because it is the first medication to target two specific receptors: GLP-1 (glucagon-like peptide-1) and GIP (glucose-dependent insulinotropic polypeptide). While previous generations of treatment focused only on one, this dual-action therapy mimics the synergistic effect of natural gut hormones more effectively.

By activating these pathways, the medication improves insulin secretion, decreases the liver’s glucose production, and slows gastric emptying. This complex interaction is what makes it a premier choice for advanced metabolic care in modern clinical settings.

The Science of Mounjaro in Dubai: How It Functions

To understand how this treatment works, one must look at the gut-brain axis. When we eat, our bodies release incretin hormones to manage the energy influx. In many patients with metabolic concerns, these signals are weakened.

Mounjaro acts as a replacement and enhancement for these signals. It tells the brain that the body is satisfied much sooner than usual and ensures that the energy from food is processed efficiently by the cells rather than being stored immediately as fat. This systematic improvement in energy utilization is the hallmark of advanced metabolic therapy.

Clinical Indications: Why This Therapy Is Prescribed

This medication is primarily used for two critical health objectives:

- Type 2 Diabetes Control: Achieving superior glycemic regulation and lowering HbA1c levels.

- Chronic Weight Management: Providing a biological tool for significant fat reduction in patients with a high BMI.

Mounjaro in Dubai is often the chosen intervention when a patient’s metabolic markers—such as fasting blood sugar or waist-to-hip ratio—indicate that lifestyle changes alone are insufficient to prevent long-term health complications.

The Spectrum of Therapeutic Benefits

Beyond the primary goal of weight reduction, patients experience a cascade of health improvements:

- Metabolic Flexibility: The body becomes better at switching between burning carbs and burning fat.

- Inflammation Reduction: Many patients see a drop in systemic inflammatory markers.

- Organ Health: Improved liver function and reduced visceral fat surrounding the heart and kidneys.

- Sustained Energy: Stable blood sugar prevents the “crashes” often associated with insulin resistance.

In our clinical experience, these internal health markers often improve significantly even before the patient reaches their final goal weight.

Who Qualifies for This Advanced Protocol

Candidacy is determined through a rigorous medical screening. Ideal candidates include:

- Individuals with a BMI of 30 or higher (Obesity).

- Individuals with a BMI of 27 or higher who have at least one weight-related condition (e.g., high blood pressure).

- Patients with Type 2 Diabetes seeking better glucose management.

- Those who have no history of medullary thyroid carcinoma or MEN 2 syndrome.

Your physician will perform a baseline blood panel to ensure your kidneys, liver, and pancreas are healthy enough to begin the titration process.

The Treatment Roadmap: A Step-by-Step Guide

The process is structured to ensure safety and long-term adherence:

- Metabolic Assessment: A deep dive into your hormonal health and weight history.

- First Injection: Performed under clinical guidance to ensure proper technique.

- Monthly Titration: The dose is gradually increased every four weeks to find your “therapeutic window.”

- Lifestyle Integration: Working with a clinical team to adjust protein intake and resistance training.

- Maintenance Planning: Developing a strategy for when you reach your target metabolic state.

The injection itself is a simple, once-weekly task that takes less than a minute, typically administered in the fatty tissue of the stomach or thigh.

Primary Targets and Expected Physical Changes

While Mounjaro in Dubai is systemic, its effects are most visible in:

- The Midsection: Significant reduction in dangerous visceral (belly) fat.

- Overall Silhouette: General slimming as the body utilizes stored fat for energy.

- Face and Neck: Often the first areas where patients notice a reduction in inflammation and fat.

- Muscle Tone: With proper protein intake, patients can achieve a leaner, healthier composition.

Financial Considerations and Treatment Value

The cost of advanced metabolic therapy involves several factors:

- The cost of the medication pens (4 doses per month).

- Clinical supervision and follow-up blood work.

- Specialized nutritional support.

- Long-term health savings from preventing chronic disease complications.

While the monthly cost is a consideration, most patients view it as a vital investment in their longevity and daily quality of life.

Navigating the Adaptation Phase

Because the medication affects the digestive system, there is an adjustment period. Most patients experience:

- Early satiety (feeling full very quickly).

- Changed taste preferences (less desire for sweets/greasy foods).

- Minor GI shifts as the stomach slows its emptying process.

What patients typically report during recovery is that these sensations are manageable and actually helpful in retraining their relationship with food portion sizes.

Safety First: Monitoring Side Effects

Safety is paramount. While most side effects are mild (nausea, constipation, or occasional fatigue), they are closely monitored. To ensure the best experience:

- Start with the lowest dose.

- Stay hydrated with electrolytes.

- Eat small, protein-focused meals.

- Report any persistent abdominal pain to your clinician immediately.

Regular follow-ups at the clinic ensure that the medication is working for you, not against you.

Sustaining Your Metabolic Gains

The ultimate goal is a “metabolic legacy”—results that last. To achieve this, we focus on:

- Protein Prioritization: To protect muscle mass during weight loss.

- Strength Training: To keep the basal metabolic rate high.

- Mindful Eating: Using the “quieted” hunger signals to learn new habits.

- Consistent Follow-ups: Adjusting the plan as your body reaches new plateaus.

Conclusion: A New Chapter in Your Health

The transition to a healthier metabolic state is a journey that requires the best of modern science and personal commitment. Mounjaro in Dubai offers a powerful, evidence-based pathway to achieving goals that may have previously felt impossible.

At Tajmeels Clinic, we specialize in guiding patients through this transformative process with expert medical oversight and compassionate care. We believe that weight management should be treated as the complex medical field it is, ensuring every patient receives a personalized strategy for success. Your health is your most valuable asset, and we are here to help you protect it.

If you are ready to explore the benefits of advanced metabolic treatment, we invite you to take the first step toward a more vibrant future.

Author

The Rise and Identity of Corteiz Clothing

Buy Lab-Certified Gemstones Online: Elora Gems 2026

Custom Earring Box Design: BoxesGen & CustomBoxesLab

The Power of Human Connection: Manual Guest Post Outreach

You Should essential hoodie Shop at hoodies Official Store

Epson Printer Troubleshooting Guide: 2026 Fixes

Cox.net Yahoo Email: Guide to Fix Login, Sync & Email Issues

Best Air Cleaners for Home: Types, Benefits, and Maintenance Tips

Canon Printer Support: Quick Ways to Contact Customer Care

Packaging Companies: Trends, Top Players & Packaging Solutions

Cybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

Team Communication Software Transforms Operations at Finance Innovate

Project Management Tool Transforms Long Island Business

How Alleviate Poverty Utilized IPPBX’s All-in-One Solution to Transform Lives in New York City

Breast Cancer: The Imperative Role of Mammograms in Screening and Early Detection

Unstoppable Collaboration: D.C.’s Citi Open and Silicon Valley Classic Unite to Propel Women’s Tennis to New Heights

Embracing Renewal: Sizdabedar Celebrations Unite Iranians in New York’s Eisenhower Park

The Benefits of Starting a Side Hustle for Financial Freedom

New Blood Donation Screening Questions What You Need to Know

Stylishly Timeless: The 5 Types of Sandals You Need in Your Closet

-

Business3 years ago

Business3 years agoCybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

-

Business3 years ago

Team Communication Software Transforms Operations at Finance Innovate

-

Business3 years ago

Project Management Tool Transforms Long Island Business

-

Business3 years ago

How Alleviate Poverty Utilized IPPBX’s All-in-One Solution to Transform Lives in New York City

-

health3 years ago

Breast Cancer: The Imperative Role of Mammograms in Screening and Early Detection

-

Sports3 years ago

Unstoppable Collaboration: D.C.’s Citi Open and Silicon Valley Classic Unite to Propel Women’s Tennis to New Heights

-

Art /Entertainment3 years ago

Embracing Renewal: Sizdabedar Celebrations Unite Iranians in New York’s Eisenhower Park

-

Finance3 years ago

The Benefits of Starting a Side Hustle for Financial Freedom