Finance

Pakistan’s Economic Crisis: Unraveling the Factors Behind the Fall

Introduction:

Pakistan’s economy finds itself in a state of crisis, facing multifaceted challenges that have contributed to its current turmoil. In this analysis, we unravel the complex factors that have led to Pakistan’s economic downturn, examining policy decisions, external pressures, and internal dynamics. Dr. Aisha EconInsight, an expert in economic matters, provides a comprehensive exploration of the roots of Pakistan’s economic crisis and Pakistan economic crisis potential avenues for recovery.

The Economic Descent:

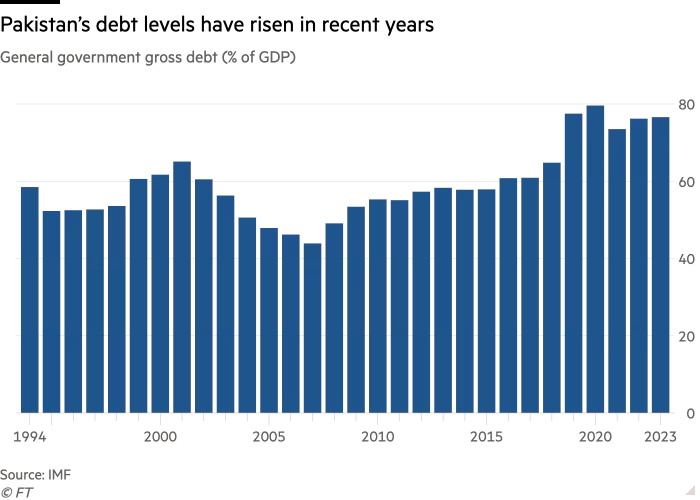

This image is taken from google.com

Explore the series of events and decisions that have contributed to Pakistan’s economic crisis. Delve into the economic indicators, policy shifts, and external factors that have played a role in the downturn.

Comparative Analysis: Economic Indicators

This image is taken from google.com

| Economic Indicator | Previous Strengths | Current Challenges | Analyzing the shifts in key economic indicators contributing to the crisis |

|---|---|---|---|

| GDP Growth | Robust Growth Rates | Stagnation and Decline | Assessing the factors behind the slowdown in GDP growth |

| External Debt | Manageable Levels | Escalating Debt Burden | Understanding the challenges posed by an increasing external debt |

| Inflation Rates | Previous Stability | Rising Inflationary Pressures | Examining the factors contributing to the surge in inflation rates |

Expert Commentary: Dr. Aisha Econ Insight’s Analysis

Benefit from Dr. Aisha Econ Insight’s expert commentary as she dissects the contributing factors to Pakistan’s economic crisis. Gain insights into the challenges faced by policymakers and potential strategies for economic recovery.

Policy Decisions and Governance

This image is taken from google.com

Delve into the role of policy decisions and governance in shaping Pakistan’s economic trajectory. Dr. Aisha EconInsight discusses the impact of policy shifts, reforms, and their effectiveness in addressing economic challenges.

External Pressures and Global Dynamics

Explore the external pressures and global dynamics influencing Pakistan’s economic crisis. Dr. Aisha EconInsight sheds light on the impact of international factors, trade relations, and geopolitical considerations.

Socio-Economic Implications

This image is taken from google.com

Analyze the socio-economic implications of the economic crisis on the people of Pakistan. Dr. Aisha EconInsight discusses the challenges faced by the population, including unemployment, poverty, and social disparities.

Pathways to Recovery

In the face of the economic crisis, explore potential pathways to recovery for Pakistan. Dr. Aisha EconInsight provides insights into strategic measures, policy adjustments, and international collaborations that could pave the way for economic stability.

Conclusion:

The economic crisis in Pakistan is a result of a confluence of factors, both internal and external, shaping the country’s economic landscape. Dr. Aisha Econ Insight’s expert analysis provides a nuanced understanding of the challenges faced by Pakistan and outlines potential avenues for recovery. Stay informed on the evolving dynamics of Pakistan’s economy with this in-depth analysis.

Author

Author

Each option serves a different purpose and works in a different way. Choosing the wrong option can increase borrowing costs, create repayment pressure, or limit flexibility. Understanding how these funding options compare helps businesses make better financial decisions.

This blog explains how collateral free loans, overdrafts, and cash credit work, their advantages and limitations, and which option may be better for different business needs.

What Is a Collateral Free Loan?

A collateral free loan is a loan where the business does not need to provide any asset or property as security. The lender approves the loan based on the business’s financial performance, credit history, and repayment capacity.

These loans are commonly used by MSMEs, startups, traders, and service providers who may not own assets or do not want to risk them.

In most cases, lenders assess:

- Business turnover

- Bank statements

- Credit score

- Repayment history

- Stability of income

Key Features of a Collateral Free Loan

- No collateral or asset pledge required

- Fixed loan amount

- Fixed repayment schedule

- Faster approval compared to traditional facilities

- Suitable for short- to medium-term funding needs

Collateral free loans are often used for working capital needs such as paying salaries, purchasing inventory, covering rent, or managing temporary cash flow gaps.

What Is an Overdraft Facility?

An overdraft facility allows a business to withdraw more money than what is available in its current account, up to a pre-approved limit. It is linked directly to the bank account and is mainly used for short-term cash needs.

Interest is charged only on the amount used, not on the entire approved limit. Overdraft limits are usually reviewed or renewed annually by banks.

Key Features of an Overdraft

- Linked to a current account

- Interest charged only on utilized amount

- Flexible withdrawals and repayments

- Usually requires collateral or strong banking history

- Annual renewal required

Overdrafts are commonly used by businesses with regular cash flow and a strong relationship with their bank.

What Is Cash Credit?

Cash credit is a working capital facility provided mainly to businesses involved in trading or manufacturing. The loan limit is usually based on stock levels and receivables.

Like overdrafts, interest is charged only on the amount used. Cash credit limits are reviewed periodically and require regular submission of financial data.

Key Features of Cash Credit

- Limit based on inventory and receivables

- Interest charged on utilized amount

- Mostly secured with collateral

- Requires frequent documentation

- Suitable for ongoing working capital needs

Cash credit facilities are widely used by medium-sized and established MSMEs.

Collateral Free Loan vs Overdraft vs Cash Credit: Key Differences

Although all three options support working capital, they differ in structure and suitability.

- Collateral Requirement: Collateral free loans do not require any asset as security. Overdraft and cash credit facilities usually require collateral or a strong banking relationship.

- Approval Time: Collateral free loans are usually approved faster. Overdraft and cash credit approvals take longer due to documentation and assessment.

- Repayment Structure: Collateral free loans have fixed repayment schedules. Overdraft and cash credit facilities allow flexible repayments without fixed instalments.

- Interest Calculation: Collateral free loans charge interest on the full loan amount. Overdraft and cash credit charge interest only on the amount used.

- Documentation: Collateral free loans require limited documentation. Overdraft and cash credit require regular financial reporting and renewals.

- Flexibility: Overdraft and cash credit offer more flexibility in usage. Collateral free loans are less flexible but more structured.

Advantages of Collateral Free Loans Compared to Overdraft and Cash Credit

Collateral free loans offer several benefits, especially for small and growing businesses.

1. No Asset Risk

Businesses do not have to pledge property or assets, reducing financial risk.

2. Faster Access to Funds

Quick approval helps manage urgent cash requirements.

3. Simple Structure

Fixed loan amount and repayment schedule make planning easier.

4. Suitable for Businesses Without Banking History

Newer businesses can access funding without long banking relationships.

5. Less Ongoing Compliance

Unlike OD and CC, there is no need for annual renewals or frequent documentation.

Advantages of Overdraft and Cash Credit Facilities

Overdraft and cash credit facilities remain useful for certain business situations.

1. High Flexibility

Businesses can withdraw and repay funds as needed.

2. Interest on Used Amount Only

This reduces interest cost when the full limit is not used.

3. Suitable for Regular Working Capital Cycles

Ideal for businesses with predictable cash inflows and outflows.

4. Long-Term Availability

Once approved, these facilities can be renewed year after year.

Which Option Is Better for Your Business?

There is no single option that suits all businesses. The right choice depends on cash flow patterns, urgency, and business stability.

A Collateral Free Loan Is Better If:

- You need funds quickly

- You do not own assets to pledge

- Your cash flow is irregular

- You prefer fixed repayments

- You want minimal documentation

An Overdraft or Cash Credit Is Better If:

- Your business has steady cash flow

- You need flexible access to funds

- You have a strong banking relationship

- You can manage regular reporting

- You want to pay interest only on used funds

Collateral Free Loan vs OD or CC for MSMEs

MSMEs often face delayed payments, seasonal demand, and limited asset ownership. Many small businesses find it difficult to meet the requirements for overdraft or cash credit facilities.

For such businesses, collateral free loans provide a practical solution. They offer faster access to funds without the need for assets or long approval processes.

Established MSMEs with stable revenue and assets may still prefer overdraft or cash credit for long-term working capital management.

Common Mistakes Businesses Make While Choosing Working Capital Options

- Choosing flexibility without considering repayment discipline

- Ignoring renewal and compliance requirements

- Overestimating cash inflows

- Using long-term facilities for short-term needs

- Not comparing total borrowing cost

Avoiding these mistakes helps maintain healthy cash flow.

Things to Consider Before Choosing Any Working Capital Facility

Before selecting a funding option, businesses should review:

- Cash Flow Pattern: Understand whether cash inflows are regular or irregular.

- Urgency of Funds: Immediate needs may require faster options.

- Cost of Borrowing: Consider interest, fees, and compliance costs.

- Operational Simplicity: Choose a structure that is easy to manage.

- Business Stability: Long-term facilities suit stable businesses better.

Final Thoughts

Collateral free loans, overdrafts, and cash credit facilities each serve a specific purpose. A collateral free loan offers speed, simplicity, and safety from asset risk, making it suitable for MSMEs and urgent needs. Overdraft and cash credit facilities provide flexibility and cost efficiency for businesses with stable cash flows and strong banking relationships.

The right option depends on business size, financial stability, and cash flow requirements. Choosing based on actual business needs, rather than habit or convenience, helps ensure better financial control and long-term stability.

FAQs

- Is a collateral free loan better than overdraft or cash credit?

It is better for businesses that need quick funds, have irregular cash flow, or do not own assets.

- Do overdraft and cash credit require collateral?

In most cases, yes. Banks usually require collateral or strong financial history.

- Which option has faster approval?

Collateral free loans usually have faster approval compared to overdraft or cash credit.

- Can businesses use more than one option?

Yes, some businesses use a combination based on different needs.

Author

Many homeowners sit on a hidden pot of money without knowing it. Your house likely gained value since you first bought it years ago. This extra value, called equity, can work as a tool for you. The bank sees this equity as real money that can be borrowed.

Current market rates play a key role in this whole process. The lower rates available today make this option worth looking into now. Your savings depend on the gap between old and new interest rates. Many people find that even small rate drops create big monthly savings. The math works out better when your home has gained good value.

Smart Approaches to Debt Consolidation Refinancing

This option works best for people with a stable income and good equity. Your first step should involve checking the current home value versus the loan balance. The gap between these numbers shows how much money you could access.

Some people wonder about using installment loans alongside refinancing strategies. These loans offer fixed terms with set payment amounts each month. Your budget becomes easier to plan when all debts follow clear payment schedules. Many installment loans cost much less than credit cards or payday loans.

What Is Real Estate Refinancing?

Your home can work as a powerful tool to tackle other money problems. The basic idea involves swapping your current mortgage for a new one with better terms. This new loan pays off your old mortgage while giving you extra cash. Many homeowners use this method to reduce their monthly payments or pull out equity.

The money from refinancing can help clear high-interest debts that drain your budget. Your credit cards or personal loans might charge rates many times higher than mortgage rates. This big rate gap creates an opportunity to save serious money each month. Most people find the process takes about a month from start to finish.

- Your monthly savings can add up to thousands over several years

- The tax benefits might make mortgage interest less costly overall

- This option works best when your home has gained good value

Who Can Refinance to Pay Off Debt?

The right to refinance depends on several factors beyond just owning a home. Your current equity position plays a major role in what options lenders offer. Most banks want to see at least 20% equity remaining after any cash-out refinance. The time you’ve owned your home also matters to many lenders.

Your income and credit history will face careful review during this process. Many people find they need scores above 620 for standard refinance options.

- Your job stability matters greatly to mortgage lenders today

- Most banks require at least two years at your current employer

- The value of your home needs formal checking through an appraisal

Pros of Using Refinancing for Debt Payoff

The main benefit comes from trading high-interest debt for much lower rates. Your credit cards might charge 18-25% while mortgage rates stay under 7% in most cases. This huge gap means each dollar works harder to clear your debts.

The stress relief from simplifying your financial life matters as much. Instead of juggling multiple due dates and different lenders each month, you have one payment. Your budget becomes easier to manage with this simpler setup.

- Most high-rate loans keep you paying mostly interest for years

- Your credit score often improves as credit card balances drop

- The total interest paid over time drops dramatically with lower rates

Types of Refinancing Options

Here are the different types of refinance loan options:

Standard Remortgage With Extra Borrowing

This common approach replaces your current mortgage with a larger new one. The extra money above what you already owe becomes cash in your pocket. Most lenders allow borrowing up to 80% of your home value through this method. Your new loan pays off the old mortgage while giving you funds to clear other debts.

- Your interest rate applies to the entire new loan amount

- Most lenders offer fixed rates from 2 to 10 years for stability

- The approval process takes about 4 to 6 weeks, typically

Second Charge Loan Secured On Home

This option lets you keep your existing mortgage while adding another loan. The second loan sits behind your main mortgage in terms of priority. Your current mortgage terms stay the same throughout this process. Many people choose this when their main mortgage has a great rate already.

- Your existing mortgage lender does not need to approve this loan

- Most second charge loans process faster than full remortgages

- The fees tend to be lower than with complete refinancing

- This works well when your current mortgage has exit penalties

Equity Release For Older Borrowers

Homeowners above age 55 can access special lifetime mortgage products. These loans let you tap home equity without making monthly payments. Your loan balance grows over time as interest adds to the original amount. Most people repay these loans when they sell their home or pass away.

- No monthly payments need to be made during your lifetime

- The interest compounds over time and adds to your loan balance

- Your home ownership stays secure throughout the loan term

- Most lenders guarantee you can never owe more than your home value

- This suits people with limited income but substantial home equity

Offset Mortgages To Manage Debt

This unique mortgage links your savings account to your home loan balance. Your savings reduce the amount of mortgage that charges interest. The unique setup helps you save interest while keeping access to your money. Many people find this useful for managing various financial goals together.

- Your savings remain accessible, but work to reduce interest costs

- The setup allows flexible overpayments without penalties

- Most offset products let you borrow back money you have overpaid

- Your mortgage rate may run slightly higher than standard options

Conclusion

High-interest loans and cards drain money from your budget each month. Your credit cards charge between twenty and thirty per cent interest yearly. Payday loans often cost even more with rates that seem unreal. The debt cycle traps many people who make payments but never progress. These high costs eat away at money that could build your future.

The bank sees your home as safer than unsecured debt types. Your property acts as backup for the loan if anything goes wrong. This safety lets banks offer much lower rates than credit card companies. Many people find they can finally see an end to their debt tunnel. The fixed payment plan helps you know exactly when your debts will clear.

Author

Understanding the Role of Assessment in Education

Can Window Tinting Improve Fuel Efficiency in Boynton Beach?

Navigating Health in a Busy World: Your Guide to Wellness

How Ceramic Coating Improves Resale Value in Long Beach

Moonga (Red Coral): Astrological Significance and Benefits

Baby Rashes: Common Types, Causes, and Care Tips

Fixing AOL Mail Crashes: Common Causes and Easy Solutions

Understanding Istikhara: Your Guide to Seeking Allah’s Guidance

Hellstar Clothing: The Bold Brand Everyone’s Talking About in 2026

AI and Automation: Transforming Business Workflows for Efficiency

Cybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

Team Communication Software Transforms Operations at Finance Innovate

Project Management Tool Transforms Long Island Business

How Alleviate Poverty Utilized IPPBX’s All-in-One Solution to Transform Lives in New York City

Breast Cancer: The Imperative Role of Mammograms in Screening and Early Detection

Unstoppable Collaboration: D.C.’s Citi Open and Silicon Valley Classic Unite to Propel Women’s Tennis to New Heights

Embracing Renewal: Sizdabedar Celebrations Unite Iranians in New York’s Eisenhower Park

The Benefits of Starting a Side Hustle for Financial Freedom

New Blood Donation Screening Questions What You Need to Know

Stylishly Timeless: The 5 Types of Sandals You Need in Your Closet

-

Business3 years ago

Business3 years agoCybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

-

Business3 years ago

Team Communication Software Transforms Operations at Finance Innovate

-

Business3 years ago

Project Management Tool Transforms Long Island Business

-

Business2 years ago

How Alleviate Poverty Utilized IPPBX’s All-in-One Solution to Transform Lives in New York City

-

health3 years ago

Breast Cancer: The Imperative Role of Mammograms in Screening and Early Detection

-

Sports3 years ago

Unstoppable Collaboration: D.C.’s Citi Open and Silicon Valley Classic Unite to Propel Women’s Tennis to New Heights

-

Art /Entertainment3 years ago

Embracing Renewal: Sizdabedar Celebrations Unite Iranians in New York’s Eisenhower Park

-

Finance3 years ago

The Benefits of Starting a Side Hustle for Financial Freedom