Finance

Blockchain Financial Security Transforming Financial Systems

By

Reviewed

By Mike steven

lockchain technology has emerged as a disruptive force in the financial industry, reshaping how we think about data, transparency, and security. At its core, blockchain operates as a decentralized ledger, recording transactions in an immutable, transparent, and secure way. The technology was initially designed to support cryptocurrencies like Bitcoin, but its potential to address security concerns within the financial sector has propelled it to the forefront of innovation. This article delves into how blockchain enhances financial security, examining its potential applications, benefits, and challenges.

Understanding Blockchain Technology

Blockchain is essentially a distributed ledger technology (DLT) where data is stored in blocks that are linked or “chained” together. These blocks are secured and verified using cryptography, ensuring that once data is added, it cannot be altered without detection. Each transaction on a blockchain is verified by a network of computers, making it secure and nearly impossible for unauthorized users to modify or falsify data.

This design has profound implications for financial security. In traditional financial systems, security is managed by central authorities, which can lead to vulnerabilities. With blockchain, the data is decentralized, meaning it is not controlled by any single entity, reducing the risks associated with centralization.

How Blockchain Enhances Financial Security

Blockchain provides a number of features that make it an ideal solution for enhancing financial security:

- Transparency and Immutability

Every transaction on a blockchain is recorded and visible to all participants within the network. This transparency ensures accountability, as all participants can verify each transaction’s authenticity. The immutability of blockchain data means that once a transaction is recorded, it cannot be changed, protecting against fraud and tampering. - Decentralization Reduces Risk

Unlike traditional systems, blockchain’s decentralized nature means there is no central point of failure. This decentralization helps to prevent breaches, as attackers would need to compromise the majority of the network to alter data—a challenging and resource-intensive task. - Enhanced Identity Protection

Blockchain offers a higher level of privacy protection by enabling participants to transact without revealing personal information. Techniques like zero-knowledge proofs allow transactions to be verified without exposing any underlying data, reducing risks of identity theft. - Efficient Fraud Detection and Prevention

Blockchain’s structure makes it difficult for unauthorized transactions to go unnoticed. Because every transaction must be verified by the network, fraudulent activities are more easily detected and prevented. This is especially valuable in combating financial crimes, such as money laundering and transaction manipulation. - Automation through Smart Contracts

Smart contracts are self-executing contracts with terms written directly into code. These contracts automate financial processes, reducing the need for intermediaries and minimizing human error and manipulation. This automation not only speeds up processes but also reduces risks associated with manual handling.

Blockchain Applications in Financial Security

The potential applications of blockchain in enhancing financial security span various sectors:

1. Banking and Payments

Blockchain allows for faster, cheaper, and more secure cross-border transactions. By eliminating intermediaries, blockchain reduces transaction costs while enhancing transparency and accountability. Banks are increasingly leveraging blockchain to prevent fraud, reduce operational costs, and improve customer experience.

2. Insurance

Insurance companies are turning to blockchain to combat fraud. By using blockchain to verify claims and store customer data, insurance firms can reduce false claims and ensure data integrity. The technology allows for faster processing and transparency, reducing the chances of tampering with policy details.

3. Identity Verification

Identity theft is a significant threat in the financial world. Blockchain-based solutions offer a secure, decentralized way to verify identities without exposing sensitive personal data. By using cryptographic techniques, blockchain ensures that only authorized parties can access sensitive data, enhancing user privacy and security.

4. Securities and Trading

Blockchain allows for quicker settlement of trades, reducing the risks associated with lengthy settlement times in securities trading. In traditional trading systems, settlement delays can increase risks for both buyers and sellers. Blockchain’s transparency also aids in regulatory compliance and reduces the potential for market manipulation.

Challenges to Implementing Blockchain for Financial Security

This image is taken from google.com

While blockchain holds immense potential, several challenges remain:

- Scalability Issues

Blockchain systems, particularly public blockchains, struggle to scale due to the computational resources needed for transaction verification. For blockchain to be viable for large-scale financial applications, solutions to improve scalability are essential. - Regulatory and Compliance Hurdles

As blockchain is still a relatively new technology, global regulatory frameworks are evolving. Financial institutions must navigate these changing regulations, which can be a complex and slow process. Compliance with existing financial regulations remains challenging in blockchain systems. - Integration with Legacy Systems

Many financial institutions use legacy systems that are not compatible with blockchain technology. Integrating blockchain into these existing systems may require significant technical investment and restructuring, which can be costly and time-consuming. - Security Risks

While blockchain is inherently secure, it is not immune to all types of attacks. For example, “51% attacks” occur when a group of miners gains majority control over a network, allowing them to alter transactions. As blockchain adoption grows, more sophisticated attacks could emerge, making continuous innovation in security essential.

Comparative Analysis of Blockchain and Traditional Financial Security Systems

Below is a comparative analysis table highlighting key differences between blockchain-based financial systems and traditional systems.

| Feature | Traditional Financial Systems | Blockchain-based Financial Systems |

|---|---|---|

| Data Storage | Centralized | Decentralized |

| Transparency | Limited (restricted to authorized personnel) | High (visible to all participants) |

| Immutability | Low (records can be altered by central authority) | High (once recorded, data cannot be changed) |

| Transaction Speed | Slower (due to intermediaries and manual checks) | Faster (due to automation and lack of intermediaries) |

| Cost of Transactions | High (fees for intermediaries) | Lower (reduced need for intermediaries) |

| Fraud Detection | Moderate (reliant on centralized monitoring) | High (transactions verified by network) |

| Identity Protection | Moderate (risk of data exposure) | High (enhanced privacy through cryptography) |

Analysis Table: Key Advantages and Limitations of Blockchain in Financial Security

| Aspect | Advantages of Blockchain | Limitations of Blockchain |

|---|---|---|

| Data Security | Data is immutable and encrypted | Vulnerable to 51% attacks on smaller networks |

| Transparency | Increases transparency in transactions | May conflict with privacy concerns in some regions |

| Cost Efficiency | Reduces costs by removing intermediaries | Initial setup and integration can be costly |

| Scalability | Suitable for real-time transactions in certain cases | Public blockchains face scalability challenges |

| Privacy and Identity | Enhanced privacy via cryptographic methods | Regulatory compliance with privacy laws is complex |

Conclusion: The Future of Blockchain in Financial Security

Blockchain’s potential to enhance financial security is substantial, offering solutions to long-standing issues in transparency, fraud prevention, and data protection. Financial institutions are increasingly recognizing the technology’s ability to revolutionize their security frameworks, though obstacles in scalability, regulation, and integration persist. Moving forward, blockchain’s success in the financial sector will likely depend on collaborative efforts among technology innovators, regulators, and financial institutions to address these challenges.

The adoption of blockchain will undoubtedly continue to accelerate, paving the way for a more secure and efficient financial ecosystem. By reinforcing security, reducing costs, and enhancing transparency, blockchain is poised to be a cornerstone of the financial industry’s future.

Author

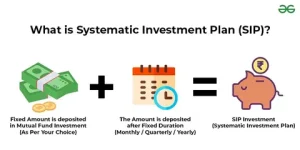

Investing in mutual funds requires strategic thinking. Smart investors constantly seek efficient paths to build long-term wealth. A Systematic Investment Plan represents one of the easiest gateways into the financial markets. Instead of deploying a massive lump sum all at once, you contribute a fixed amount at regular intervals. Most market participants select a monthly schedule. However, certain mutual fund companies also provide a daily contribution option. This choice frequently sparks a compelling debate among retail investors. Both options facilitate regular investing, but they operate on distinct operational timelines. Understanding these operational differences empowers you to make a confident financial choice. Furthermore, examining market mechanics helps you secure a prosperous future.

The Power of Rupee Cost Averaging

Systematic investing introduces a powerful mechanism called rupee cost averaging. When market prices drop, your fixed contribution purchases more units. Conversely, when markets surge, your fixed amount buys fewer units. This dynamic automatically lowers your average purchase cost over time. You eliminate the stressful guesswork of market timing. Investors no longer need to predict market bottoms or tops. Instead, automated contributions smooth out market volatility effortlessly. Market fluctuations actually work in your favor when you maintain a steady contribution rhythm.

Exploring the Mechanics of Monthly Contributions

A monthly systematic plan automates your wealth-building journey completely. The banking system deducts a predetermined amount from your account precisely once every month. You select the exact debit date that matches your financial calendar. For example, you might allocate five thousand rupees every month. The platform invests this full amount on your chosen date without delay. You receive a specific number of units based on the Net Asset Value on that trading day. Monthly schedules dominate the market because they harmonize seamlessly with standard employment salary cycles. Furthermore, investors appreciate how simple it is to track a single monthly transaction on their bank statements. Managing household cash flows becomes remarkably straightforward with a monthly rhythm.

Examining Daily Investment Strategies and Execution

Daily systematic plans function similarly, but they alter the execution frequency dramatically. Instead of a single monthly deduction, the platform executes transactions on every single business day. Suppose you wish to invest five thousand rupees over a monthly cycle. The system divides this total sum into smaller fractional portions. It deploys these micro-portions across every business day of the month. Because market prices fluctuate daily, the Net Asset Value shifts constantly. Consequently, you purchase varying quantities of fund units with each transaction. Selected mutual fund houses offer this feature for individuals who prefer hyper-frequent capital allocations. Technical systems handle these frequent debits seamlessly in the background.

Comparing Operational Frequency: Monthly Versus Daily Systems

The primary distinction between these two options involves operational frequency. A monthly plan deploys your entire capital allocation in one concentrated burst. Conversely, a daily plan distributes that exact same capital across multiple business days. Naturally, a daily schedule generates a much higher volume of transaction records every month. Nevertheless, both systems operate completely automatically once you complete the initial registration process.

Many market commentators claim that daily investing generates superior returns. They argue that spreading purchases across more market levels lowers overall risk. However, historical data invalidates this common assumption. Over extended timeframes, monthly and daily plans produce remarkably similar long-term returns. Market realities rarely favor high-frequency contribution schedules over simple monthly routines.

Dispelling Return Myths and Performance Drivers

Portfolio performance relies on entirely different operational drivers. The specific fund you choose dictates your growth trajectory far more than transaction frequency. Furthermore, broader macroeconomic conditions and your overall investment horizon dictate your final results. Simply increasing transaction frequency does not guarantee enhanced profitability. Market volatility affects all portfolios equally over long holding periods. Therefore, obsessing over daily versus monthly schedules distracts from core wealth-building principles. Successful investing requires patience, disciplined budgeting, and strategic asset allocation rather than tactical frequency tweaks. Expert fund managers emphasize asset quality over transaction timing.

Weighing Convenience and Income Alignment Factors

Convenience remains a critical pillar of personal finance management. Monthly plans offer unmatched simplicity and align perfectly with how employers disburse salaries. Managing a single monthly deduction requires minimal cognitive effort. Daily plans appeal to niche investors who desire hyper-frequent capital deployment. However, daily schedules complicate portfolio tracking and bank statement analysis. Most retail investors find that monthly structures eliminate unnecessary administrative friction. Streamlining your financial life preserves mental energy for other important life tasks. Clear financial records reduce anxiety during tax season and annual reviews.

Navigating Behavioral Finance and Emotional Discipline

Human psychology plays a massive role in successful investing. Emotional panic often triggers poor financial decisions during sudden market downturns. Automated contribution plans remove human emotion from the equation entirely. Whether you choose a monthly or daily schedule, automation enforces strict discipline. You continue buying units even when market news looks bleak. This unwavering consistency separates winning investors from panicked speculators. Trusting the automated process protects your portfolio from emotional interference. Mental resilience fuels long-term financial success.

Selecting the Ideal Systematic Plan for Your Portfolio

Every investor must determine the best approach for their unique financial situation. For the vast majority of individuals, a monthly plan serves as the most practical vehicle. It requires almost zero ongoing maintenance after initial setup. Conversely, a daily schedule works for investors who embrace high-frequency tracking and complex portfolio layouts. Ultimately, investment frequency should never serve as your primary decision criterion. Focus instead on selecting top-tier mutual funds that match your risk tolerance. Allocate a sustainable monthly budget that honors your living expenses. Sound financial planning starts with realistic goals and disciplined execution.

Achieving Long-Term Financial Success Through Consistency

Both monthly and daily systematic plans empower individuals to invest consistently. The core difference simply involves the timing of your capital deployment. Monthly options deploy funds once per cycle, while daily options spread contributions across business days. For most everyday participants, monthly structures deliver optimal convenience and ease of management.

Daily structures accommodate specific preferences, but they rarely create magical return advantages. True financial success stems from disciplined consistency and long-term commitment. Focus on staying invested through market cycles rather than worrying about the exact frequency of your automated contributions. Building lasting wealth is a marathon, not a sprint. Your future self will thank you for maintaining steady financial habits.

Author

If you need help with your Robinhood account, knowing how to contact Robinhood immediately can save valuable time. Whether you have a question about a transaction, trouble logging in, an account restriction, a cash transfer, or another account issue, Robinhood provides several ways to reach its support team. The fastest option for many customers is 24/7 in-app chat support. Robinhood also provides a callback option through its support tools for eligible issues. If you cannot access your account, there are additional steps you can take to request assistance. This guide explains the quickest ways to contact Robinhood and what information you should have ready before contacting support.

How to Contact Robinhood Immediately

Robinhood’s official support options are available through its mobile app and website. The company recommends starting with its Help Center and support tools rather than relying on contact information found elsewhere online. For the fastest response, follow these steps:

- Open the official Robinhood app or visit the Robinhood website.

- Sign in to your account if possible.

- Open Support or the Help Center.

- Select the topic that best matches your problem.

- Choose the available contact option.

- Start a chat or request a phone call back when the option is available.

Robinhood currently states that chat support is available 24/7, making it one of the most convenient ways to get help at any time.

Contact Robinhood Through 24/7 Chat

If your goal is to reach Robinhood as quickly as possible, in-app chat is usually the most convenient starting point. Robinhood offers 24/7 chat support, allowing customers to connect with support regardless of the time of day. You can also provide relevant information, screenshots, documents, or links when necessary to explain your issue. To begin:

- Open the Robinhood app.

- Go to your account or support section.

- Select the appropriate help topic.

- Choose the contact option.

- Start a support chat.

Chat can be useful for questions involving account access, transactions, deposits, withdrawals, cards, investing features, and other Robinhood products. You can also access support through Robinhood’s website if you prefer using a computer.

Request a Robinhood Phone Callback

Customers who prefer speaking with a representative can request a callback through Robinhood’s support tools. Rather than manually searching for a number, Robinhood’s current support process lets eligible customers request a call from within the app or website. After you request a callback, Robinhood says it will notify you when an agent is available and provide information about the number that will call you.

This is particularly useful when you have a complicated account question that may be easier to explain verbally. Keep in mind that not every inquiry is eligible for phone support, and availability can depend on the type of issue. Robinhood’s current support page also notes specific phone-support hours for certain investing-related inquiries.

What to Do If You Cannot Log In

If you’re searching for how to contact Robinhood immediately because you can’t log in, start by checking the login assistance options. On the Robinhood login page, select Help and choose the relevant option if you forgot your password or email address. Robinhood provides identity-verification steps to help customers regain access. If you still cannot access your account, Robinhood provides additional support options. The company says customers without account access can email support for help with freezing an account when necessary.

If you believe there is unusual activity on your account, acting quickly is important. Robinhood recommends contacting Support immediately and can provide account-freezing assistance where appropriate.

Contact Robinhood If You Notice Unusual Account Activity

If you notice a login, transaction, device, or other account activity that you don’t recognize, don’t wait to seek help. The first step is to access Robinhood directly through the official app or website. From there, contact Support and explain what you noticed. Robinhood recommends contacting support immediately if you believe your account has been compromised. Depending on the situation, you may be able to freeze the account to restrict certain activity while Robinhood reviews the situation. You should also consider changing your password and reviewing devices connected to your account. Robinhood recommends using a strong, unique password and removing devices you don’t recognize.

Have Your Information Ready Before Contacting Robinhood

If you want to resolve an issue quickly, prepare the relevant information before starting your support request. Depending on the problem, you may need:

- The email address associated with your Robinhood account

- A description of the problem

- The approximate date and time of the issue

- Relevant transaction details

- Screenshots showing an error message

- Information about the device or browser you’re using

- Details about a deposit, withdrawal, transfer, or trade

- Any relevant support case information

Avoid including unnecessary sensitive information in a message. Robinhood states that it will not ask for your password, two-factor authentication code, or secret recovery phrase. A clear explanation can help the support team understand the problem without requiring multiple follow-up questions.

Use the Correct Support Option for Your Robinhood Product

Robinhood has different products, and some have dedicated support resources. For example, Robinhood’s current support information lists dedicated assistance for products including Robinhood Crypto, Robinhood Spending, Robinhood Cash Card, Robinhood Wallet, and Gold Card. If your question concerns a specific product, selecting that product within the Support area can help direct your request to the appropriate team.

For Robinhood Wallet, the company provides a dedicated support email. For certain card-related products, Robinhood also provides specific phone support options. Because support procedures can change, it is best to check Robinhood’s current Help Center for the latest instructions before contacting the company.

Contact Robinhood Through Its Official Website

If you don’t want to use the mobile app, you can access Robinhood Support from the web. Go directly to the Robinhood website and open the Help Center. You can search for your issue, review available solutions, and use the contact options provided for your specific situation. Using the official support portal is especially helpful because Robinhood’s support options can differ depending on your account, product, and issue.

24/7 Support

Robinhood provides 24/7 chat support through its official support channels, allowing users to get assistance at any time. However, phone callback availability may vary depending on the type of inquiry and the support options available for your account.

Contact a Representative

To connect with a Robinhood representative, visit the Support section through the Robinhood app or website. After selecting the issue you need assistance with, you may see an option to request a phone call back. The availability of this option depends on the nature of your request.

Fast Support Options

For many users, the quickest way to receive help is by accessing Robinhood Support and using the 24/7 chat feature. If your concern is eligible for phone assistance, you can request a callback through the same support process.

Account Access Help

If you cannot access your Robinhood account, use the Help option on the login page and follow the required identity verification steps. If you continue to experience login problems, Robinhood provides additional support options to help you recover access to your account.

Phone Support

Robinhood offers phone support through its support process, where eligible customers can request a callback. However, phone assistance is not available for every type of inquiry and the options provided may depend on the specific issue you are trying to resolve.

Final Thoughts

If you need to contact Robinhood immediately, the best place to begin is the official Robinhood app or website. Start with the Help Center, choose the topic related to your problem, and use 24/7 chat or request a callback if that option is available. For login problems or unusual account activity, take action promptly and follow Robinhood’s official account-security instructions. Having the relevant details ready can also make the support process more efficient.

Most importantly, always access Robinhood Support directly through the official app or website. This helps ensure that you’re using the current support process and receiving assistance through the appropriate channel.

Author

Dubai attracts millions of ambitious entrepreneurs every single year. You probably know the city for its tall towers and modern lifestyle. However, Dubai offers much more than luxury living. It stands as a global powerhouse for commercial growth. Buying a company here is no longer a distant dream. In fact, it represents a smart move for savvy investors.

The local economy continues to expand at a rapid pace. Government leaders actively support foreign investors with modern regulations. Therefore, acquiring an existing venture gives you immediate access to a thriving market. You do not need to build everything from scratch. Instead, you can step into an operational setup and generate profits right away.

Why Dubai is the Ultimate Investment Destination

Dubai stands at the intersection of the East and the West. This prime geographic location allows companies to connect easily with global markets. Consequently, international trade flows smoothly through the city. In addition, the business environment offers incredible advantages. Consider the following key perks:

- Tax Benefits: Investors enjoy zero personal income tax and highly competitive corporate tax rates.

- Full Ownership: You can retain 100% foreign ownership in most commercial sectors.

- Legal Transparency: Clear laws protect your financial assets and legal rights.

- Strong Economy: A dynamic population creates constant demand for modern services.

Furthermore, the city welcomes millions of tourists each year. These visitors possess high purchasing power. As a result, consumer demand remains consistently strong across multiple sectors.

The Strategic Advantage of Buying an Existing Business

Starting a brand-new firm always carries significant risk. You must spend months securing licenses, finding staff, and hunting for customers. Conversely, purchasing an established company eliminates many of these early hurdles. First, an existing enterprise already generates regular revenue. You gain immediate access to an active customer base from day one. Second, the business already employs trained staff members. Thus, you save valuable time on recruiting and onboarding. Third, the firm possesses established supplier networks and operational systems. You simply take over the steering wheel and drive the venture forward.

Six Essential Steps to Buy a Business in Dubai

If you want to enter the Dubai market successfully, you must follow a structured approach. Careful preparation will always protect your capital.

Define Your Goals and Scope

Start by outlining your exact investment targets. Decide whether you want passive income or an active management role. Next, set a clear financial budget. Determine if you require full ownership or if you prefer a strategic partnership.

Conduct Deep Market Research

You must analyze the latest local industry trends. Demand is soaring for green technologies, digital solutions, and health services. Therefore, align your financial investments with growing market needs. Avoid declining sectors and focus on scalable industries.

Hire Qualified Local Experts

Do not navigate the local landscape alone. Instead, partner with licensed corporate brokers, legal consultants, and tax advisors. These professionals understand the subtle details of local regulations. Furthermore, they will guide you toward genuine listings and protect your interests.

Execute Thorough Due Diligence

You must inspect the target company with great care. Review all financial statements, debt obligations, and tax filings. Examine legal contracts, operational licenses, and employee agreements. Consequently, this step ensures that you do not inherit hidden liabilities.

Choose the Right Legal Structure

Dubai provides different operational jurisdictions. You can choose between Mainland, Free Zone, and Offshore setups. Each option carries specific ownership guidelines, tax rules, and geographical operational limits. Selecting the right structure directly impacts your future expansion plans. Therefore, evaluate your long-term business goals before making a final choice.

Transfer Ownership and Licenses

Once both parties agree on terms, you can finalize the purchase agreement. Next, you will transfer the official commercial licenses through government departments. The local authorities handle these legal procedures quickly. In fact, you can complete the entire process within a few short weeks.

Hot Sectors for Smart Acquisitions

To maximize your returns, focus on high-growth industries. The following sectors consistently demonstrate strong financial performance:

Tourism and Hospitality

Dubai remains a top global travel destination. Therefore, restaurants, boutique hotels, travel agencies, and luxury spas enjoy constant customer traffic. Purchasing an active hospitality venture gives you instant access to steady income.

Healthcare and Wellness

The demand for quality health services continues to rise rapidly. Local residents prioritize wellness, fitness, and aesthetic treatments. Thus, acquiring medical clinics, specialty centers, or gym facilities offers incredible stability.

Retail and E-Commerce

The local population loves shopping. Prime brick-and-mortar retail locations in popular malls yield high profit margins. Simultaneously e-commerce platforms are growing fast. Modern consumers demand fast online shopping experiences. Buying an established e-commerce setup allows you to tap into this digital shift.

Where to Find Verified Opportunities

Finding legitimate assets for acquisition requires the right sources. You should search through trusted commercial channels:

- Certified Business Brokers: Professional agencies maintain pre-screened databases of companies for sale.

- Commercial Portals: Online platforms showcase verified business listings across various price points.

- Industry Events: Business expos provide direct access to company owners and investors.

- Professional Networks: Local lawyers and accountants often know about off-market deals.

Always work with verified advisors. They verify the authenticity of seller claims and guarantee transparent financial negotiations.

Take the First Step Today

Dubai is much more than a regional financial center. It serves as a launchpad for your long-term international success. The local government continually introduces investor-friendly reforms. Consequently, the business environment remains secure, profitable, and ready for expansion. Buying an existing company offers the fastest route to commercial success. You skip the early struggles of startup life. Instead, you step straight into a running, profitable machine. Explore the vast range of opportunities today. Your next major investment milestone begins right here in Dubai.

Author

Essentials Hoodie: Premium Comfort Meets Timeless Streetwear

Carsicko Clothing UK: Modern Streetwear for Everyday Style

Mommy Makeover in Dubai for Lasting Body Contouring Results

True Religion: Premium Denim & Streetwear Style Guide

Best Franchise Businesses in Australia for First-Time Investors

IT Asset Disposition Services for Secure Data: Equipment Recovery

Vuori Clothing: Why Modern Shoppers Love This Athleisure Brand

Mahjong in Boston: Best Places for Beginners to Learn & Play

MoD vigil 200 MG for Students: Sleep Disorder Treatment Guide

HVAC Estimating Services for Accurate Project Budgeting

Cybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

Meet the Megalodon: The Shark Star of ‘Meg 2’

Reduce Video Game Lag: Level Up Your Gaming Performance

Balancing India’s Entertainment: Cricket vs. Bollywood

Jetsetter’s Secrets: Unveiling Our Favorite Travel Hacks for a Seamless Adventure

The 5 Best Live Sports Streaming Sites: Legal and Exciting!

Hollywood Labor Unrest: The Impact of ‘What About Us?’ Strikes

Unveiling the Magic of Dream Fulfillment at the Late NBA Draft

Illuminate Your Skin: Dr. Axe Unveils Natural Remedies for Lightening Knees and Elbows

Bright Choices: Navigating the Pros and Cons of Skin Whitening Creams with Dr. Axe

-

Business3 years ago

Business3 years agoCybersecurity Consulting Company SequelNet Provides Critical IT Support Services to Medical Billing Firm, Medical Optimum

-

Entertainment3 years ago

Meet the Megalodon: The Shark Star of ‘Meg 2’

-

Entertainment3 years ago

Reduce Video Game Lag: Level Up Your Gaming Performance

-

Sports3 years ago

Sports3 years agoBalancing India’s Entertainment: Cricket vs. Bollywood

-

Entertainment3 years ago

Jetsetter’s Secrets: Unveiling Our Favorite Travel Hacks for a Seamless Adventure

-

Productivity3 years ago

The 5 Best Live Sports Streaming Sites: Legal and Exciting!

-

Art /Entertainment3 years ago

Hollywood Labor Unrest: The Impact of ‘What About Us?’ Strikes

-

Sports3 years ago

Unveiling the Magic of Dream Fulfillment at the Late NBA Draft